Chart of the Day

China’s official PMIs moved in opposite directions in September: the manufacturing index fell to 49.6, while the services PMI increased to 53.2. The strong rebound in the services PMI back above 50 implies output is expanding again, following the temporary Covid restrictions that weighed on activity in August. The drop in the manufacturing PMI looks more worrying as it now implies output is contracting, even before any fallout from the Evergrande crisis and before the worst of the power shortages that have rippled through the country in the past week.

Macro

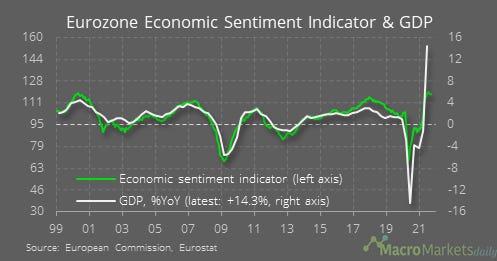

Despite the weakness in the German Ifo, the eurozone ESI rose ever so slightly in September.

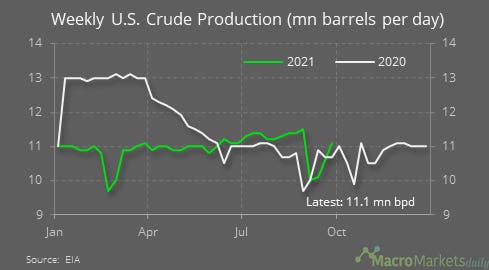

The weekly EIA report showed an unexpected rise in crude oil inventories last week, of 4.6 mn barrels – they are still below the seasonal average from the three years before Covid hit.

The unexpected rise in inventories reflected a strong recovery in production following the earlier hit from Hurricane Ida.

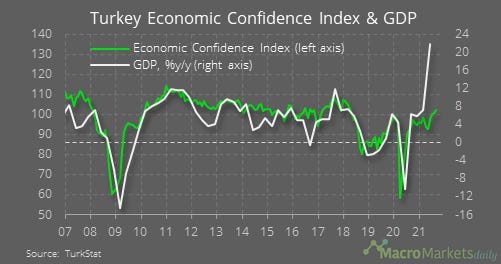

Turkey appears to be benefiting from the weak lira – the ESI there is the strongest since 2018.

Markets

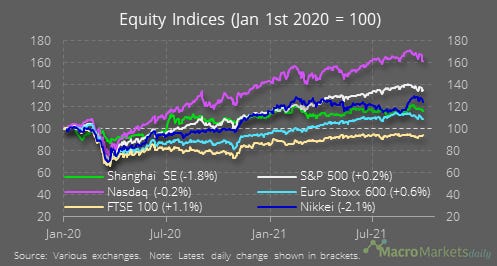

The Asian equity indices caught down up the US ones in trading yesterday. Closer to home, stocks struggled to find much momentum, with the S&P 500 and Nasdaq moving in opposite directions even as bond yields took a breather from their recent sharp upward trend.

While stocks stabilized, the USD continued to make gains against other currencies, with EURUSD briefly dipping below $1.16.

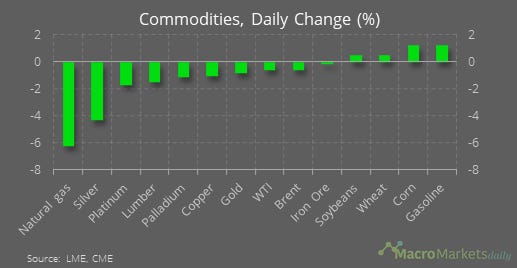

Silver slumped by 4% yesterday, meaning it has dropped through all support points seen since July, a potentially concerning signal of more weakness ahead.

It was generally a bad for commodities, though some good news for consumers as the rise in oil production appears to have contributed to a drop in natural gas prices (which is a byproduct of shale drilling). Having said that, crude took the news quite well.

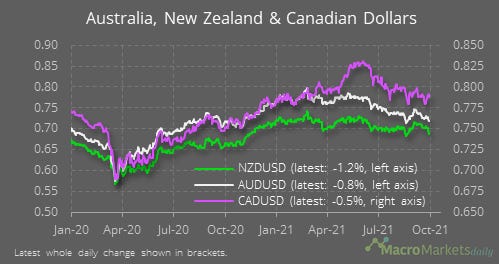

In the commodities complex, the relative strength of oil has seen the CAD outperform other major commodity currencies like the AUD and NZD – the latter fell especially sharply yesterday.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily