Chart of the Day

The big news of yesterday was the US inflation data, but as you’ve probably seen that already we’ll need with the latest China credit data instead. After a positive few months for the six-month credit impulse, it dropped back in December to close to zero. That means the flow of credit has been unchanged relatively to GDP in the past six months, not normally a great thing in terms of the outlook for various assets such as industrial metals. The 12-month impulse inched up again but remained negative. It will also move back to zero in the coming months but that’s because the decline in the flow of credit in China that happened early last year will drop out of the equation. For now, then, there is no sign yet that China is opening the credit taps despite its economic slowdown related to the property market.

Macro

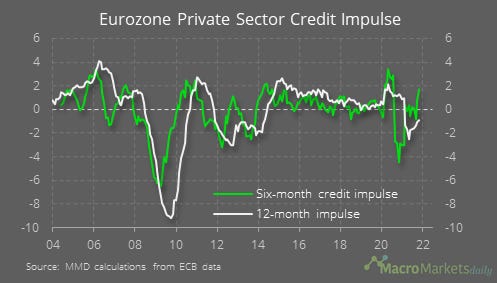

The eurozone credit impulse is getting interesting, rising sharply on a six-month basis.

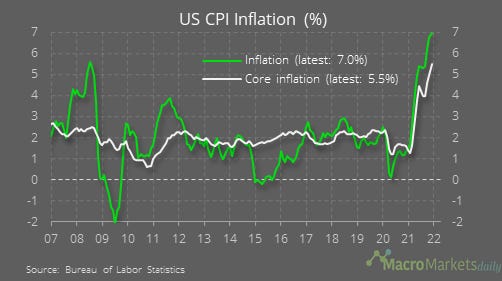

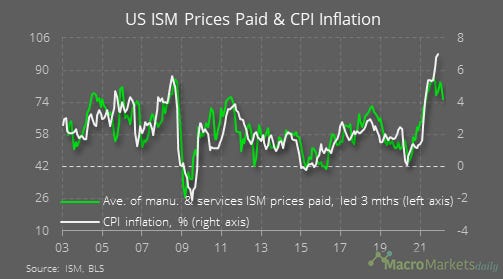

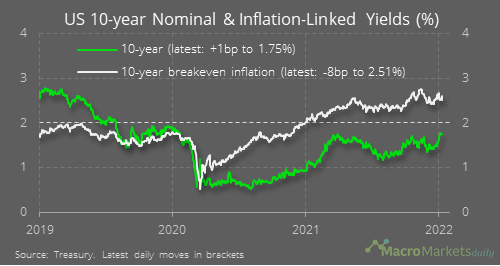

US inflation hit 7.0%. More importantly, core inflation was once again higher than economists expected (when will they learn?).

The rise in inflation means it moved further away from the rate suggested by the most recent surveys, although most believe that inflation has either peaked or will do so in January or February.

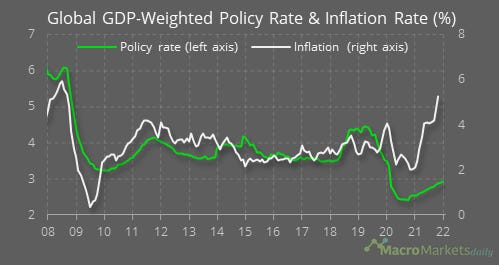

Either way you look at it, central banks seem behind the curve, not just in the US but globally too.

In the eurozone, industrial production rose by 2.3% MoM in November, but annual growth was still negative as the region’s manufacturing sector struggles with shortages.

US 30-year mortgage rates, inverse on this chart, have risen sharply in the past couple of months back to 3.5%. Will mortgage applications follow?

Markets

Bond investors shrugged off the inflation, with 10-year yields little changed in the US and falling in Europe. Canada’s rose again, perhaps because investors think the BoC will hike later this month.

Under the surface, the 10-year year breakeven rate even fell yesterday, perhaps as some peoples’ worst fears about inflation were not realized.

In the UK, expectations for BoE policy continue to increase.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily