Chart of the Day

China’s latest trade data showed export growth increased to 25.6% YoY in August, while import growth increased to 33.1% YoY. That news was well-received by economists, who thought growth in both would come in about 8%-points lower than those figures. The stronger-than-expected rises in trade appear to be a sign that supply constraints in China are easing, which would make sense given a major port re-opened last month. But this comes at a time when Covid is still flaring up across the region more broadly, and it seems global supply constraints will still be with us for several more months.

Macro

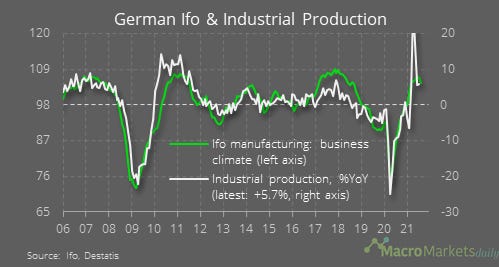

German industrial production growth increased by 1.0% MoM in July, another sign supply constraints appear to be easing. The Ifo manufacturing index there remains fairly high – in other words, demand is strong, even if supply can’t keep up.

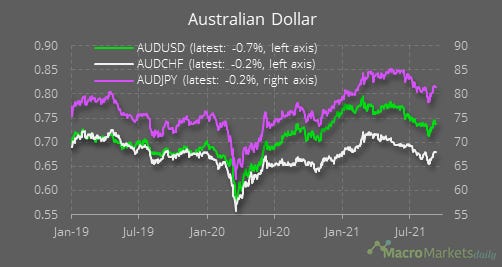

The Reserve Bank of Australia kept its policy rate unchanged but moved ahead with tapering. This wasn’t that hawkish though, because it also extended its timeframe for continuing QE into next year.

Markets

That QE extension may explains why the AUD softened yesterday after a few days of strong gains.

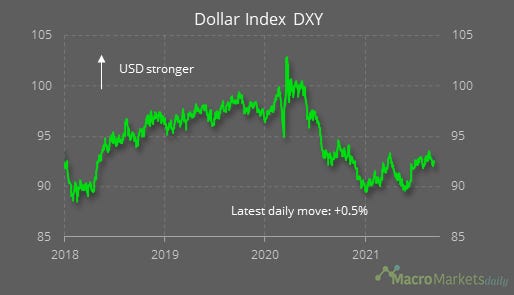

The larger fall in the AUD against the USD reflected broader USD strength, with the DXY up 0.5% but still weaker than a few weeks ago.

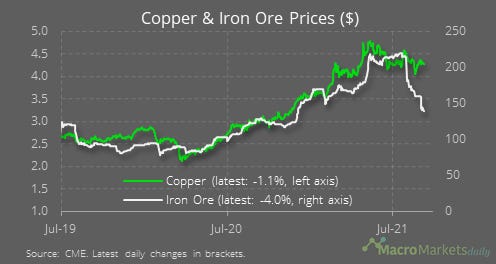

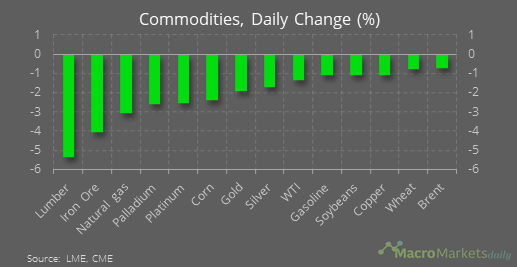

Some of the weakness in AUD, and the other commodity currencies, was due to further falls in those commodity prices. Iron, one of AUstralia’s key exports, dropped another 4%.

And it was a weak day across the board.

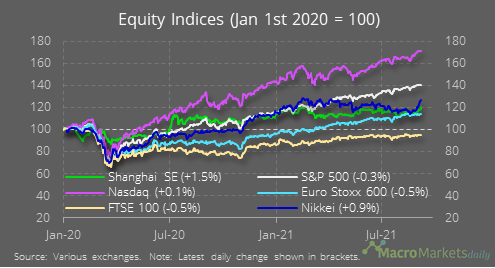

While the moves in commodities look ominous, there have been some strong outperformances from some regional equity markets. The Nikkei and Shanghai indices have both turned up again lately.

Likewise, so has the main Indian index. By contrast, Brazilian equities are still lagging amid political concerns in Brazil.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily