Chart of the Day

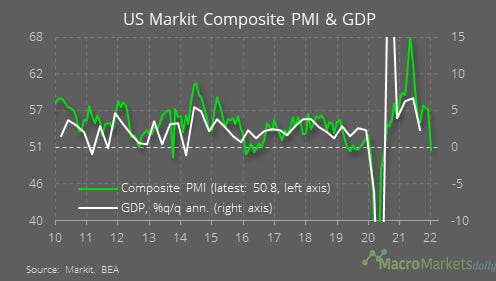

The US Composite PMI fell by 6.2 points in January to an 18-month low of just 50.8. Technically, that is higher than the 50.0 mark that supposedly separates expansion from contraction, although on a long-run basis it still looks consistent with flat GDP growth. While that is bad news for the short-term economic outlook, the news appeared to contribute toward a repricing of interest rate expectations with less chance of the Federal Reserve pulling a surprise rate hike on Wednesday, and may therefore have counterintuitively contributed to the rebound in equity markets yesterday.

Macro

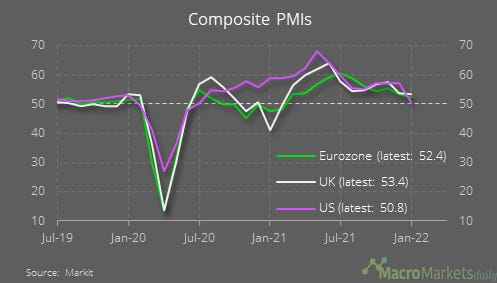

The January PMIs held up better in Europe.

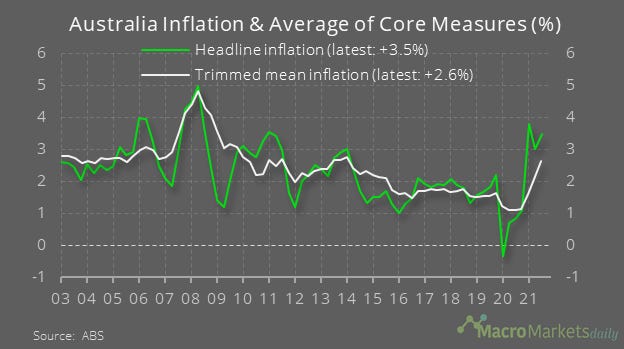

Australian core inflation jumped to the highest in years in Q4, though it is still low by US standards.

Markets

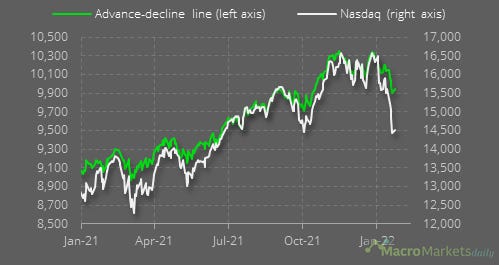

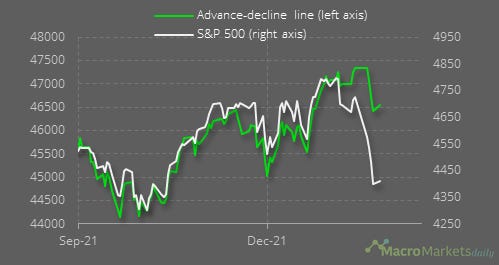

After suffering a decline of more than 3% intraday, the Nasdaq closed up slightly, and the rebound in the advance-decline line shows that a majority of firms increased on the day.

Similar dynamics were at play for the S&P 500.

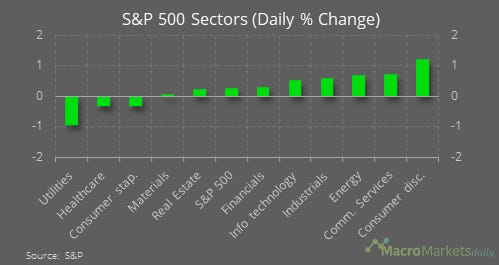

Encouragingly, all of the main defensive sectors underperformed. Tech stocks benefited from the drop in real yields following the weak PMI, but cyclicals like industrials and energy also did well.

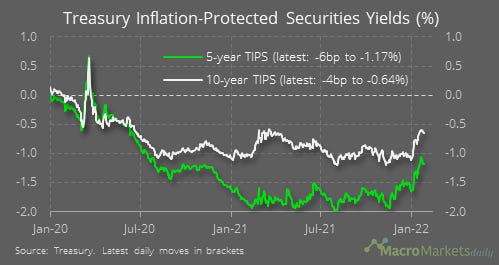

The drop in real yields was largest at the short end, as traders reduced their expectations for near-term policy tightening.

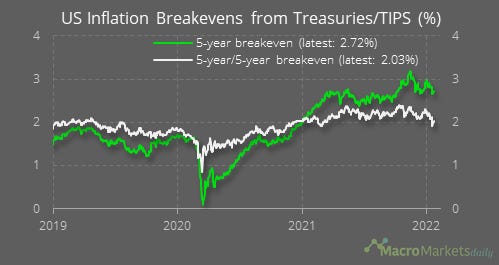

One interesting question is whether the Fed would want to get much more hawkish from here when the 5-year/5-year inflation breakeven rate, a rough proxy for markets’ inflation expectations (as it also contains other components like a liquidity premium) has already dropped back to 2.0%.

Gold has performed relatively well in the past couple of weeks even as real interest rates have jumped.

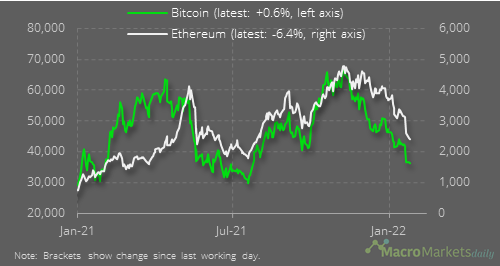

Will crypto also enjoy a rebound after its large sell-off?

Like what you see? Please forward this email to your friends and colleagues and tell them to sign up at www.macromarketsdaily.com, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily