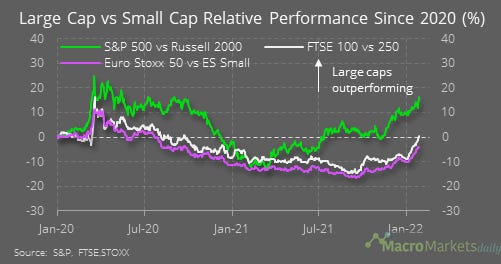

Chart of the Day

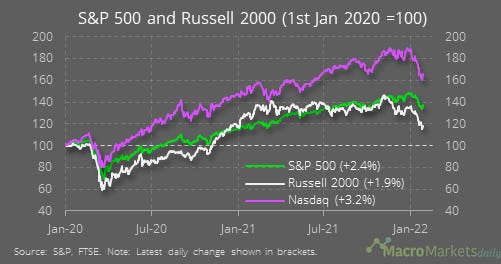

Across the US, eurozone and UK, large-cap stocks have been doing much better than their small-cap equivalents so far this year. There are a couple of plausible reasons for that, including the theory that small caps will be hit hardest by rising interest rates and/or inflation, because they lack the pricing power that some of their larger peers enjoy. However, the speed of the move, which is not dissimilar to that in early 2020 during the pandemic sell-off, also suggests a role for market liquidity. During market sell-offs, sellers of small stocks with lower liquidity are forced to accept much lower prices to offload them. If there is a liquidity effect at play, then there could be some key buying opportunities once markets calm down.

Macro

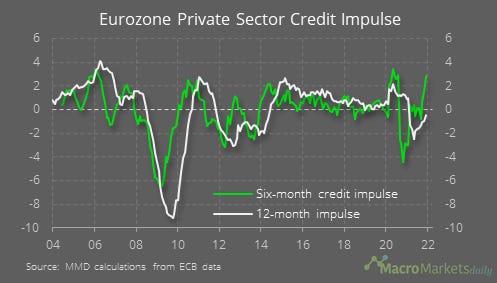

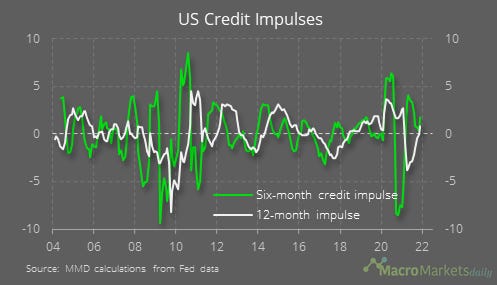

In the eurozone, the credit impulse improved further in December, normally a good sign for the outlook.

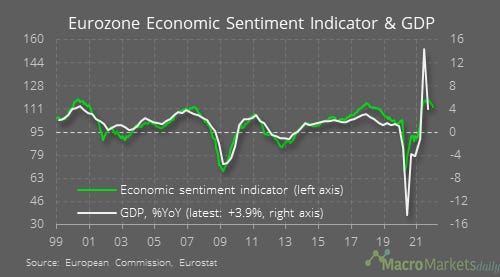

The business surveys are not as positive though, with the ESI falling in January.

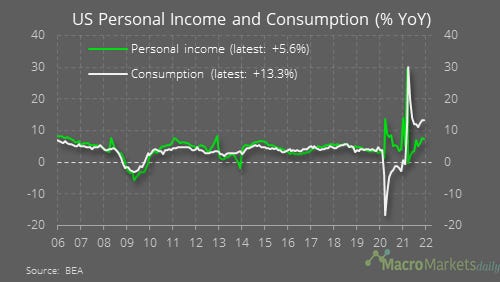

The US personal income and spending data for December showed income growth slowed to 5.6% YoY, while consumption growth was 13.3% YoY.

The gap between income and spending in the US is also partly explained by rising credit growth.

Markets

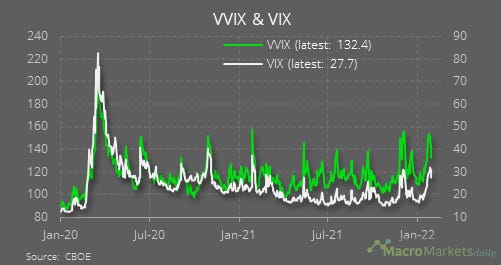

The VIX has started to drop back again.

The Russell’s gains since 2020 are now down to less than 20%, so less than one-third of the gain for the Nasdaq.

One concerning sign for equity investors is that credit spreads are widening again.

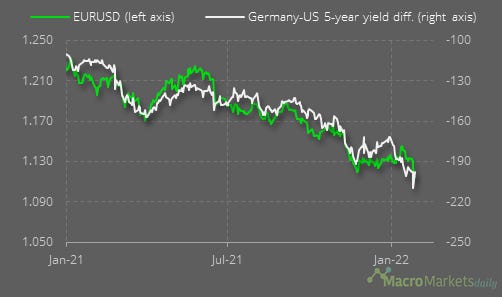

The euro finally “caught down” with relative interest rates last week, as it dropped to $1.114

Like what you see? Please forward this email to your friends and colleagues and tell them to sign up at www.macromarketsdaily.com, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily