Happy new year! If you’re glad the newsletter is back, then please let a friend or colleague know by forwarding on this email and letting them know to sign up at www.macromarketsdaily.com. Thanks!

Chart of the Day

The big story of 2021 was the sharp rise in inflation and the big story of 2022 could be that it comes down swiftly again. That appears to be the message from the ISM manufacturing survey, as the prices paid component fell by much more than economists expected in December, implying inflation could fall to around 3% later this year. If that were to occur – and it is still a big if given the disruption from Omicron could put further upward pressure on supply chains – then there would be less pressure on the Fed to tighten policy. That in turn could set the stage for another strong year for equities. Before we jump to any conclusions though, we need to see how the price components of the ISM services survey developed in December. That data is out on Thursday.

Macro

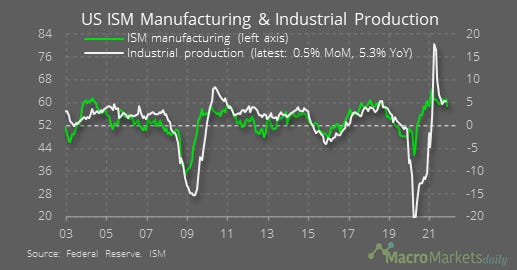

The headline US ISM manufacturing index fell to 58.7 in December, which left it consistent with industrial production growth of around 4% YoY, a little weaker than in November.

The new orders less inventories spread rebounded in December, but its low level implies the headline manufacturing ISM could decline sharply in the coming months. The logic is that, with inventories now rising, firms won’t need to order as much in the future.

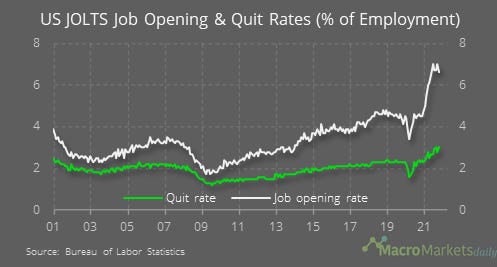

The Job Openings and Labor Turnover Survey showed that the job openings rate was unchanged at 6.6% in November, while the quit rate rose to 3.0%. In other words, the labour market still looks very hot as we head into 2022.

Markets

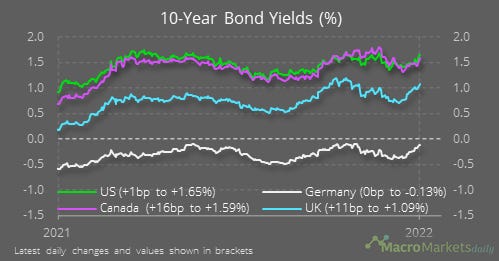

While growth stocks have been hit in the past week, thereby weighing on the US major stock indices, the European bourses have generally done much better.

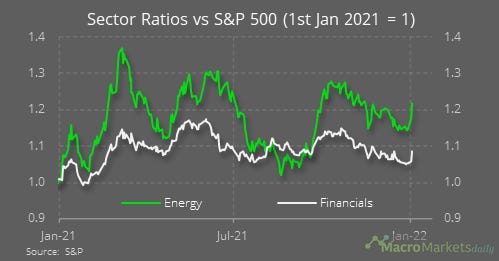

The energy and financial sectors have both made strong starts to the year, with the energy sector up by 7% in two days. Relative to the broader market, though, that only takes both sectors back to where they were a few months ago

The weakness of tech/growth stocks in recent days partly reflects the relative sharp rises in bond yields.

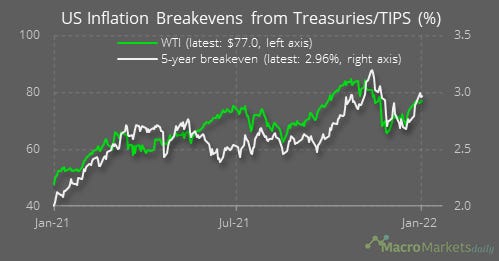

5-year inflation breakevens have been rising again, alongside oil prices.

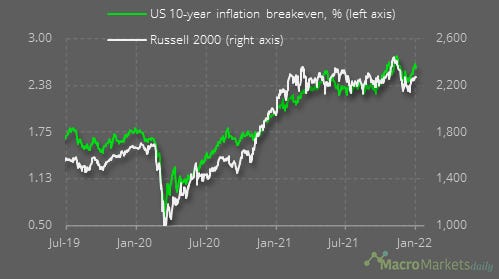

The rise in inflation breakevens may herald more upside for the Russell, though its not a particularly strong signal so far.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily