Chart of the Day

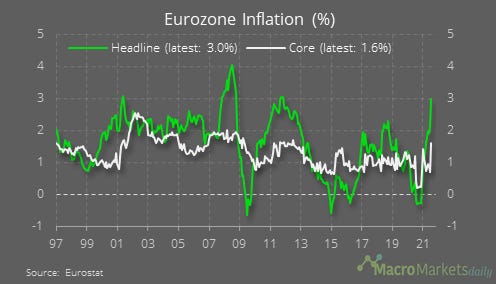

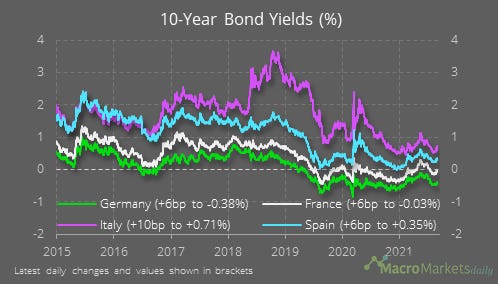

One of the key data releases yesterday came out of the eurozone, where inflation jumped by more than expected in August, to 3%. The ECB will be paying closer attention to core inflation, which excludes energy and food prices, which was still below its official 2% target, at 1.6%. Nonetheless, the increase was larger than expected and has prompted speculation that the ECB will soon start to think about tapering its asset purchases, which led to upward pressure on eurozone bond yields yesterday.

Macro

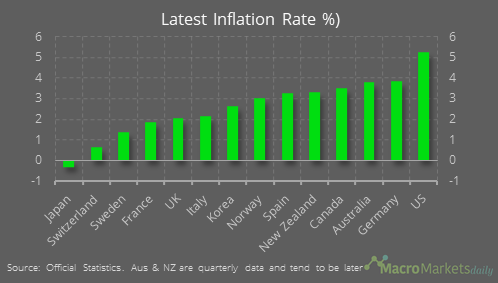

While high for the eurozone, the 3% inflation rate is much lower than the 5.1% rate in the US.

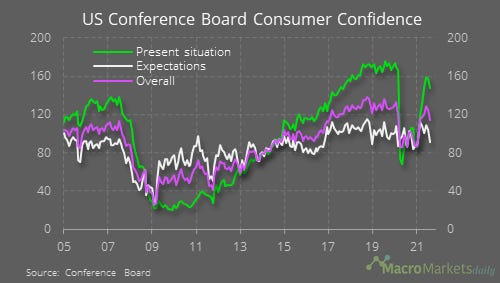

The US Conference Board measure of consumer confidence fell sharply in August. Consumers’ expectations and assessment of the present situation both deteriorated, with their economic expectations especially weak.

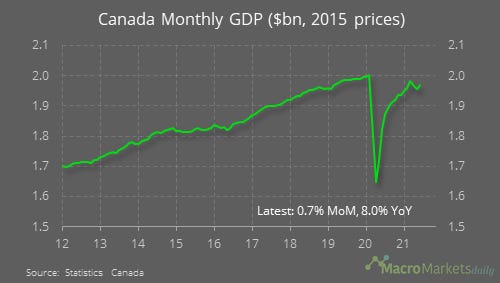

Canada’s GDP fell in Q2, which no one seemed to expect despite the lockdowns there. On a monthly basis, GDP did rise in June.

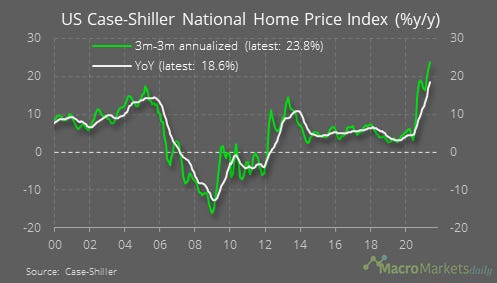

US house price inflation accelerated to 18.6% in June. Over the past three months, annualized house price growth has been even stronger at 23.8%, showing there is still strong momentum.

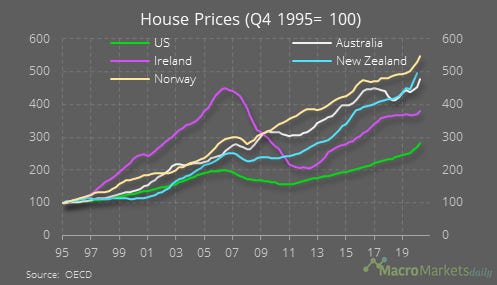

On a historical basis, the OECD data show house price growth has lagged other countries (this only goes to Q1).

Markets

10-year yields across the eurozone generally rose yesterday. Lots of attention on Italy at the moment where they are rising the most, and where concerns about fiscal sustainability tend to be highest.

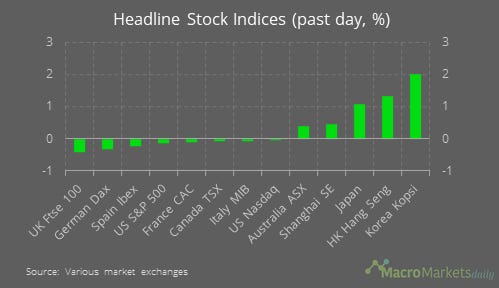

Speculation about ECB tapering may help to explain some of the declines in European stock indices, although it was generally a weak day in non-Asian markets.

Trends in Korean export growth have been following developments in the MSCI equity index this year.

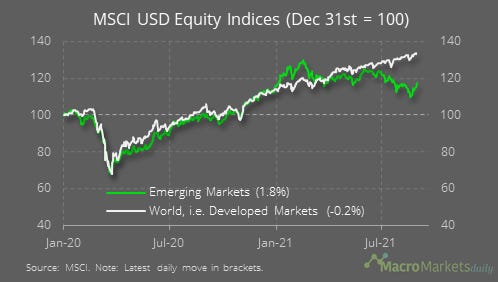

The MSCI emerging markets index rose by 1.8% yesterday and is closing the gap with the developed market index, as equities in China rebound.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily