Chart of the Day

The US Conference Board measure of consumer confidence unexpectedly fell in September. Consumers’ expectations and assessment of the present situation both deteriorated, which means their expectations are now the lowest since the 2020 lockdowns. The weakness of consumer confidence is likely linked to the sharp rise in prices so far this year, with higher gasoline prices often closely on consumers’ minds. The weak data may also have contributed to the sharp fall in equities yesterday, although the further rise in bond yields was probably the main factor.

Macro

US house price inflation accelerated to 19.7% in July, although the fall in the 3m-3m rate shows momentum is starting to fade.

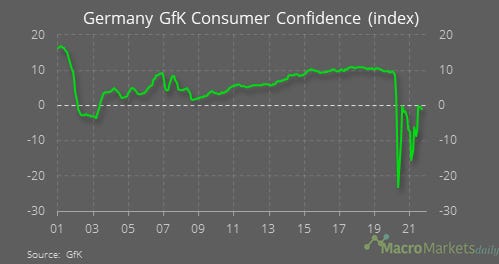

German consumer confidence also fell in September, and remains relatively low.

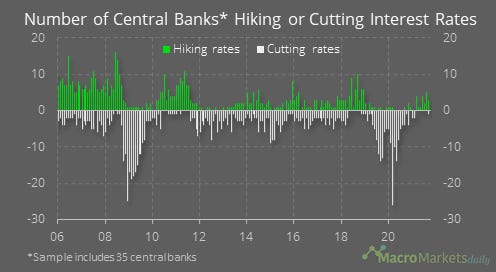

Central banks are beginning to raise rates again.

Markets

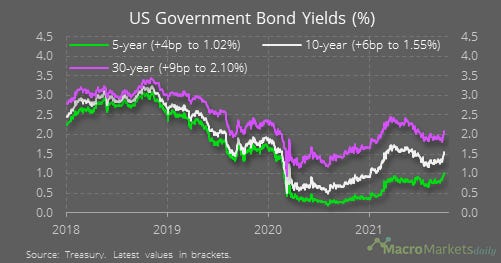

Those hikes, and hawkish messages from other CBs, have contributed to the sharp rise in bond yields. The US 10-year yield has risen by 22 bp in the past week, the 5-year has risen by 19 bp and the 30-year has risen by 24 bp.

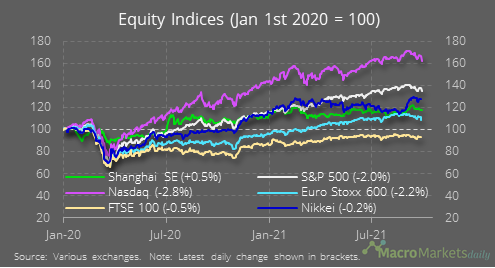

That was bad news for equity markets yesterday – the weakest was a 2.8% fall for the Nasdaq, which tends to be most sensitive to rate changes.

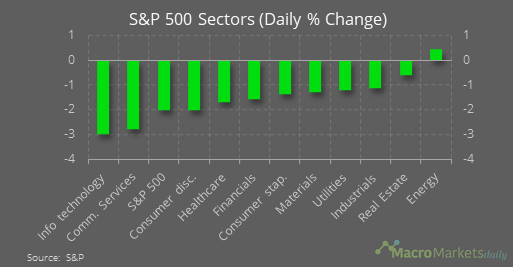

Similarly, it was tech stocks that dragged the S&P 500 down – most sectors outperformed the index yesterday, but still fell.

Higher yields have helped boost the ratio of financials to the S&P 500 – though financials still weakened yesterday.

Higher bond yields have seen the USD start rising again.

One major loser in FX markets has been the GBP. Despite the hawkish signal from the BoE last week, it’s also fallen against the euro – most are blaming some major supply issues there which will weigh on GDP.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily