Chart of the Day

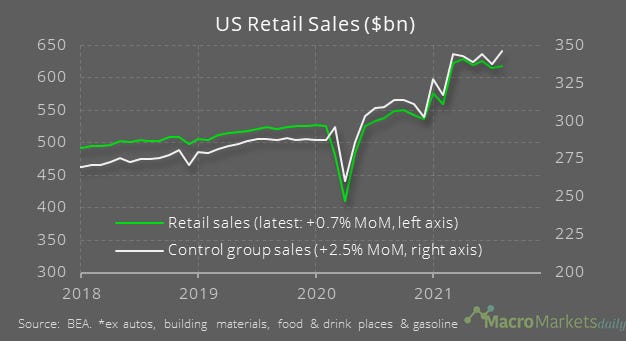

The old adage is “don’t bet against the US consumer” and that was the case yesterday, as the data showed US retail sales rose 0.7% MoM in August, which went against the economist forecast of a decline. Control group retail sales – which feed into the GDP data for consumption – rose by a strong 2.5% MoM. While you might think this is good news for markets as it shows the US economy is stronger than economists thought, we’re in a bit of an opposite world at the moment where good data can be bad news for markets because it increases the chance of the Fed tightening policy, and therefore pushes up interest rates, which can be bad news for stocks. Yesterday, all the major US equity indices were pretty much unchanged.

Macro

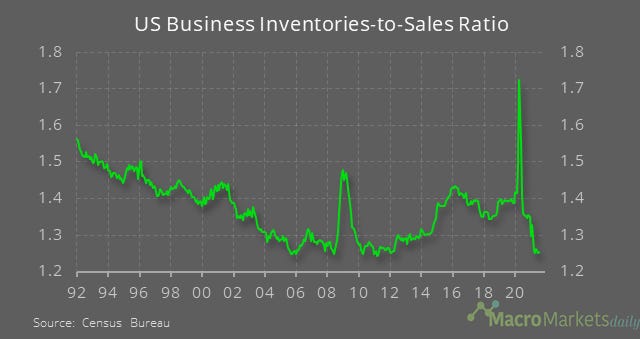

The other data showed the business inventories-to-sales ratio was still very low in July. Low inventories could presage more upward movements in prices.

The eurozone goods trade balance rose to 1.3% of GDP in July. Its currently being held down by the supply problems in the car sector, which is holding back Germany’s exports.

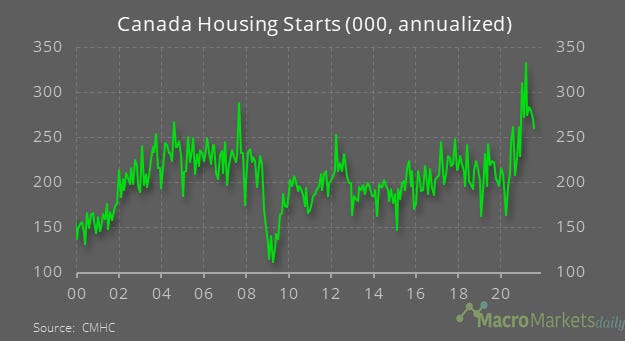

In Canada, housing starts fell to 260,000 annualized in August, down from 271,000 the previous month, but still higher than before Covid hit.

Markets

No wonder when Canadian house prices are risen by even more than in other countries lately.

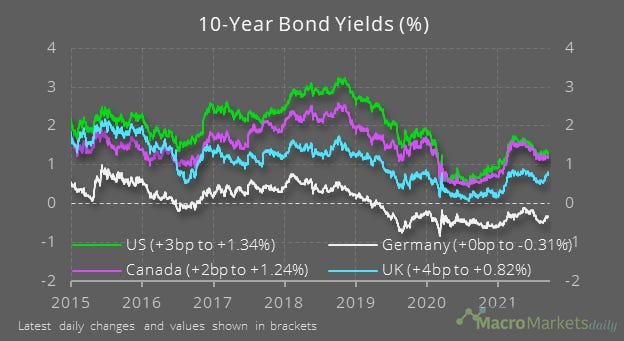

The US data contributed to a bit of upward pressure on bond yields. Lately, they have risen by the most in the UK.

The 2-year yield spread between the UK and US might normally be consistent with a stronger GBP.

Higher bond yields may help to explain why equities failed to make further ground.

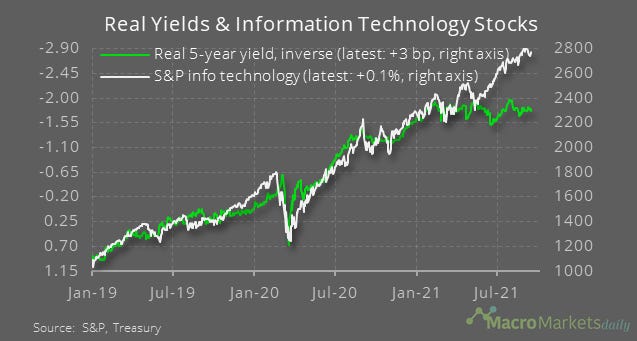

Tech stocks look especially vulnerable if bond yields rise further – there was a strong link between yields and tech stocks, until recently.

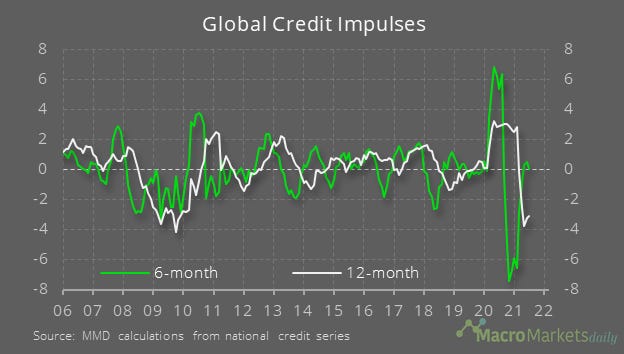

While some investors fear the Fed tapering, the weak levels of the global credit impulses would normally be a factoring keeping yields down.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily