Chart of the Day

Yesterday, the Fed signalled that it is likely to announce its QE taper in November, and half of FOMC members now think interest rates will be increased in 2022. That caused a mixed reaction in bond markets. The more hawkish message caused yields to rise on bonds at the short end of the curve, with the 5-year yield edging up by 2bp. But yields fell further out on the curve, mostly due to lower inflation breakevens. That’s because investors now think the Fed will be tougher on inflation.

Macro

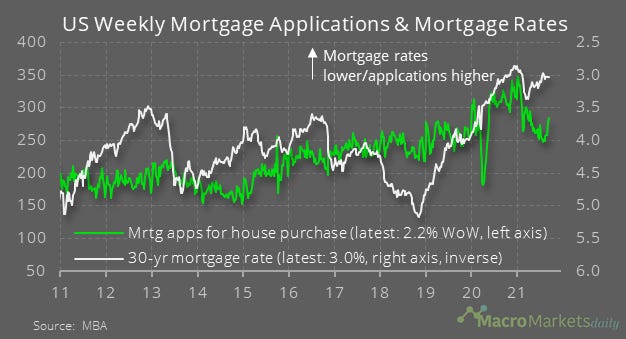

In the US, mortgage applications for house purchase have risen sharply in recent weeks, despite little change in mortgage rates.

Markets

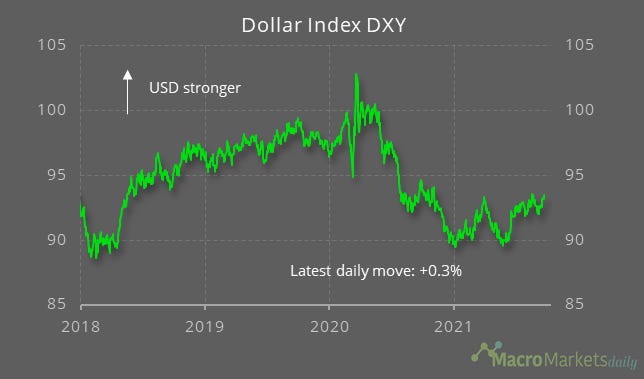

The Dollar Index also rose after the Fed meeting – traders will be looking to see if it can surpass its recent peak.

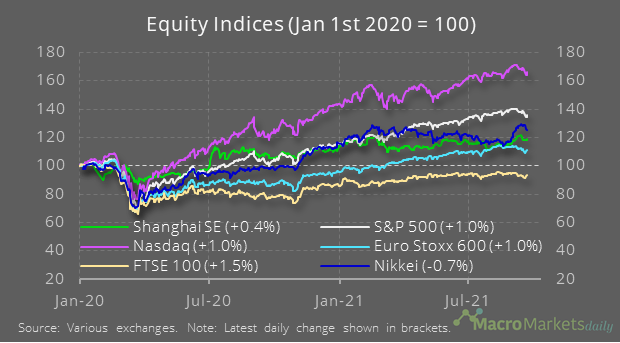

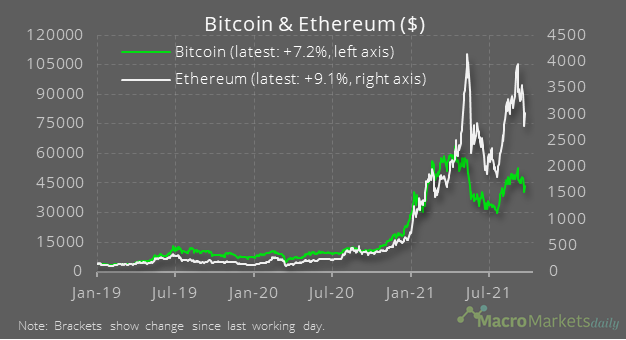

Despite the more hawkish message from the Fed, equity markets staged a modest recovery, as China injected funds into its monetary systems to try to fend off liquidity concerns.

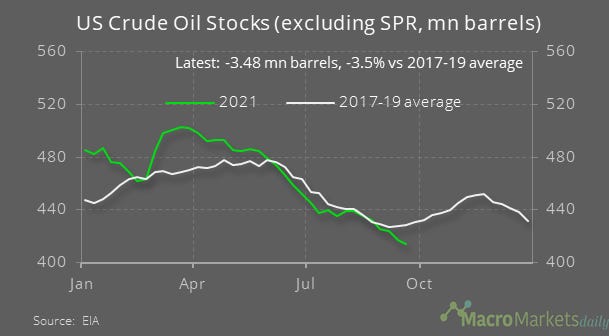

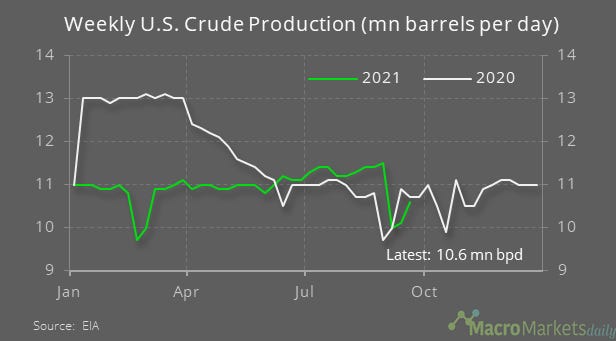

The weekly EIA report showed crude inventories fell by 3.5 mn barrels last week and are now 3.5% lower than their average at this time of year over 2017-19.

That’s because production has yet to recover from the Hurricane Ina damage.

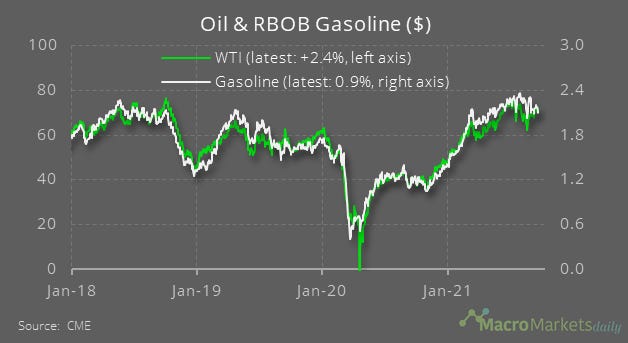

Conversely, gasoline stocks unexpectedly rose sharply.

The decline in crude stocks caused oil prices to rise by more than gasoline prices.

The broader market rebound was a big help to platinum and palladium.

Similarly, the main cryptos recouped some of their losses.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily