Didn’t get a chance to do this late last week so here is a special weekend edition. The next newsletter will be in early January – happy holidays to all!

Chart of the Day

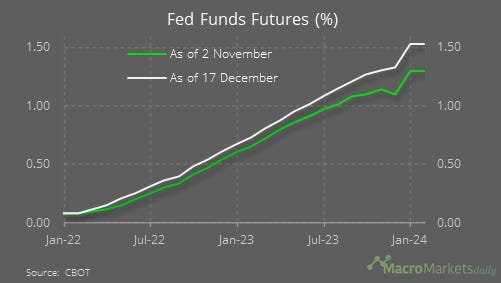

The big events late last week were the various central bank meetings, with most turning more hawkish, and the Fed in particular presenting a much more hawkish set of dot-plot projections. The median projection is now that the fed funds rate will be 1.6% by the end of 2023 and 2.1% by the end of 2024. As this chart shows, that is a bit more hawkish than fed funds futures imply, suggesting investors do not think the Fed will be able to tighten that significantly. That is maybe because investors feel that many rate hikes would damage the economy. While they might be right, the risk is that such damage is necessary to bring inflation back down again, if the current high rate is sustained for much longer.

Macro

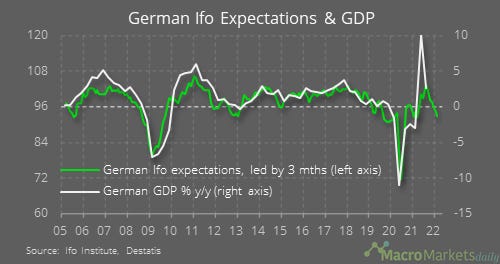

The German Ifo survey expectations component fell to 92.6 in December, leaving it consistent with negative GDP growth.

Markets

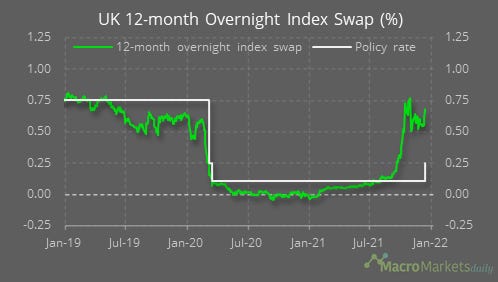

The Bank of England hiked its policy rate to 0.25% last week – the 12-month OIS rate points to further tightening ahead.

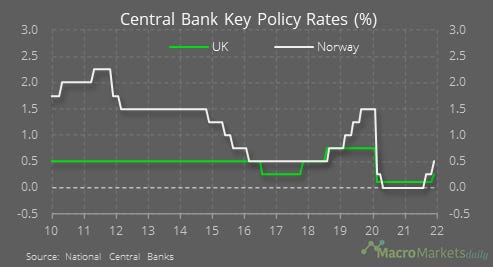

As well as the BoE, the Norges Bank also hiked last week – to 0.5%.

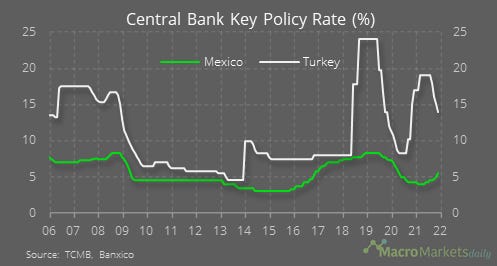

The decision by the Turkish central bank to cut rates, by 100 bp, stands out versus other EM central banks, with Mexico’s CB hiking last week to 5.5%.

The hawkish shift from the Fed last week contributed to a rise in the USD – though the dollar index is still lower than it was earlier this year.

While the rate hike from the Mexican central bank last week helped support the peso, the Turkish lira continued to tumble.

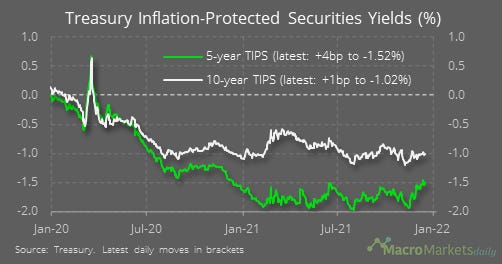

Despite the hawkish shift from the Fed last week, real bond yields were little changed.

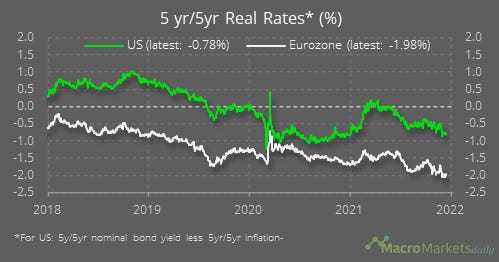

Real long-term interest rates remain deeply negative, and have drifted down in the US and eurozone despite some hawkish CB signs.

The hawkish CB moves and Omicron spread contributed to the weakness in the S&P 500 last week – might it bounce off its 50-day moving average again?

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily