Chart of the Day

The big move in markets yesterday was the further decline in US bond yields, with the 10-year yield closing below 1.5%. As you’ll see below, the recent decline in US bond yields has been a story of falling inflation expectations. While markets are not always right, the recent moves suggest we should take seriously the idea that the current rise in consumer price inflation will only be transitory. If anything, at this point the Fed might start to become concerned about yields being too low given broader economic conditions, rather than too high.

Macro

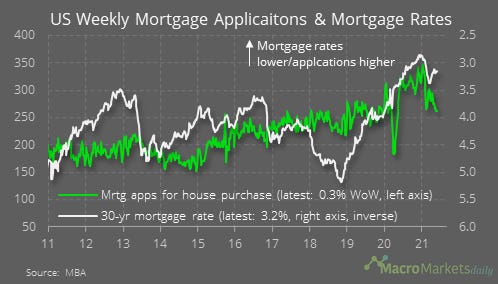

Much of the hear has gone from the housing market – mortgage applications for house purchase are now back at pre-Covid levels.

The weekly EIA report showed crude inventories below their norm for this time of year – no wonder oil prices have been rising.

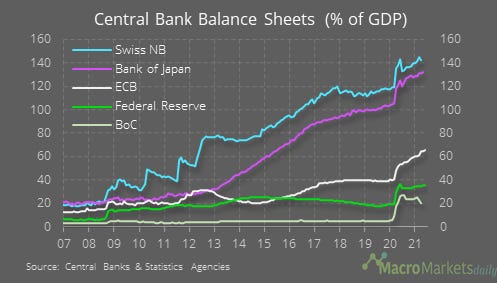

The Bank of Canada held policy unchanged yesterday. Recently, its balance sheet has been declining as a share of GDP.

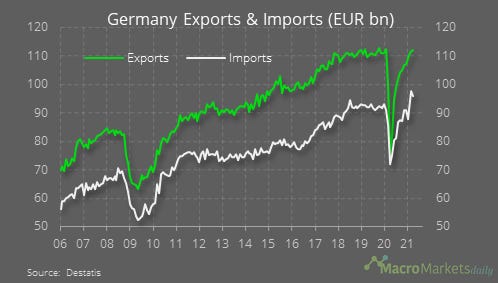

Germany exports are now back to pre-Covid levels. Imports are much higher still.

Markets

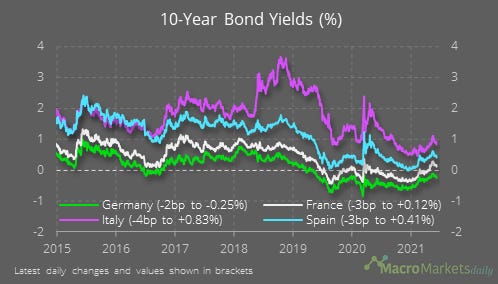

10-year yields across the world also fell yesterday. In the eurozone, over the past month, moves have ranged from a fall of 7bp in Spain to a decrease of 4bp in Germany.

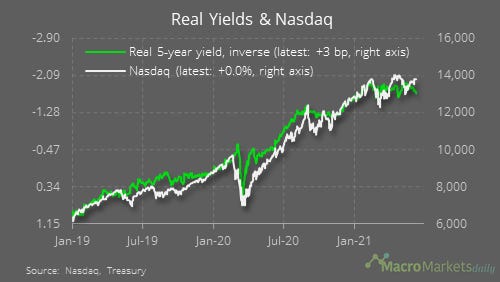

Real TIPS yields have actually been edging ever so slightly higher lately – all the decline has been from the breakeven inflation rate.

Given real yields have been little changed, there hasn’t been much of a positive impulse for tech stocks.

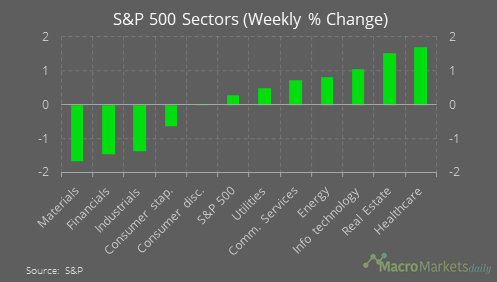

Within the equity market, some normally defensive plays – healthcare and utility – have been outperforming the broader market, while some of the most cyclicals, like materials, have been doing poorly – another sign that investors are losing faith in the relation trade.

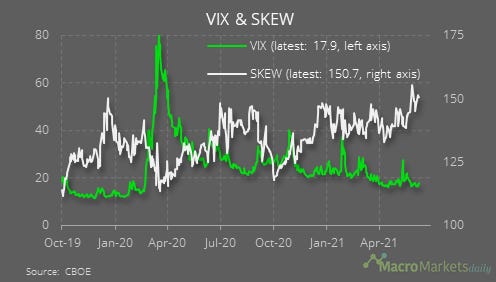

Investors still seemed to be concerned about the risk of a big sell-off – the SKEW index remains relatively high.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily

Got a question? You can reply directly to this email to get in contact.