Happy Friday! If you’re enjoying the newsletter, please do us a big favor and send this email on to some friends and colleagues.

Chart of the Day

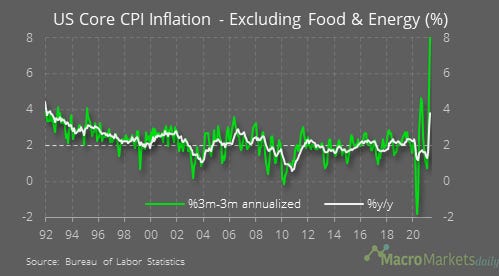

The big news yesterday was the US CPI data and the news that core inflation rose by more than economists expected, to 3.9%. That was the highest since 1992. On top of that, the three-month annualized rate surged to 8%, by far the highest in decades. That’s telling us that it’s not just base effects from the falls in prices last year that are driving inflation higher, but rather recent price pressures.

Macro

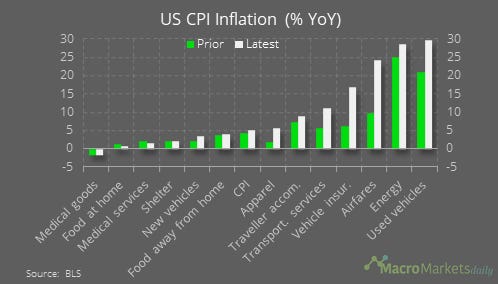

Inflation picked up in most categories, especially those linked to the re-opening.

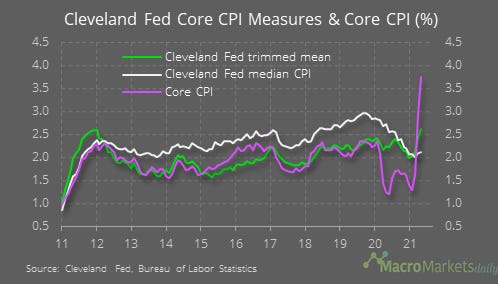

Some point to the Cleveland Fed’s core measures as evidence that this is just transitory and caused by a few big price rises. These measures strip out volatile components and are much lower than the overall core rate – they are still above the Fed’s target of 2% though.

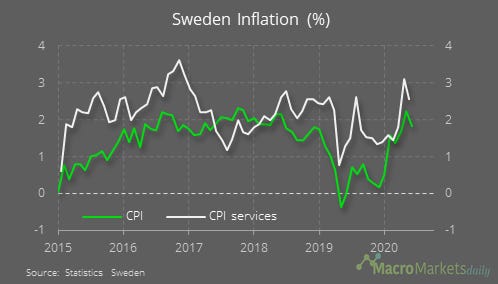

The rise in US inflation stands out internationally – for example, there was data yesterday for Sweden which showed inflation there already dropping back in May.

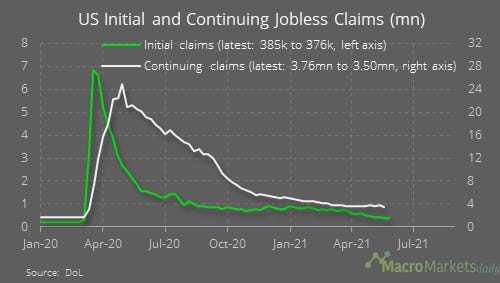

US initial jobless claims fell to 376,000 last week, while continuing claims increased to 3.5mn in the week before.

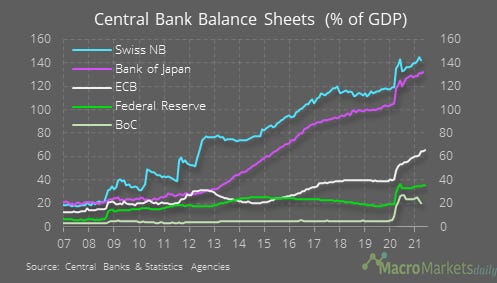

The ECB met yesterday. It was a bit of a snoozefest, with no big announcements, but the ECB confirmed it will continue to grow its balance sheet at a faster rate than most CBs.

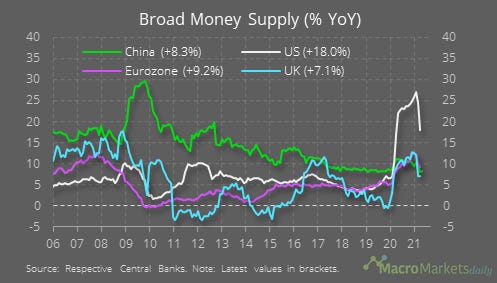

China’s money supply data showed growth on par with advanced economies – normally it is higher.

Markets

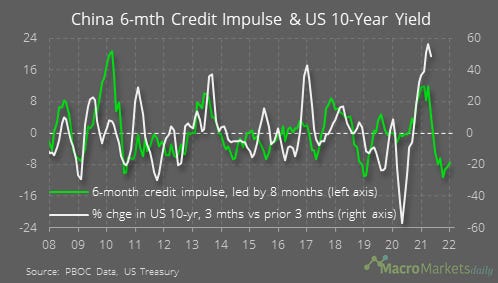

Despite stronger-than-expected inflation, the US 10-year fell. The drop was entirely due to a fall in real yields, so markets definitely do think high inflation will cause the Fed to adjust its dovish course any time soon.

It could be that developments elsewhere are keeping US yields from rising – China’s credit impulse has been pointing in that direction for a while.

FX markets appeared to react to the fall in real rates rather than the inflation data, with the USD falling against most currencies.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily

Got a question? You can reply directly to this email to get in contact.