Chart of the Day

The renewed momentum in the US equity market has owed a lot to a sharp rise in call volumes outstanding, which are now close to their previous peaks seen in 2020 and earlier this year. Around those peaks, the S&P 500 subsequently corrected as outstanding call volume dropped back again, which caused dealers to cut their positions in the stocks they were using to hedge their option books. Those corrections were nothing major in the grand scheme of things, but do suggest the market could be vulnerable to another downside move in the coming weeks.

Macro

The slowdown in China may be spreading elsewhere, with Japan’s export growth down sharply in September – also as a result of the drop in vehicle production.

The leading index there is now pointing to very weak growth, similar to the surveys in Germany, another leading vehicle maker.

Despite some bad news in Asia and for the eurozone lately, the economic surprise indices for the US and UK have been improving.

Markets

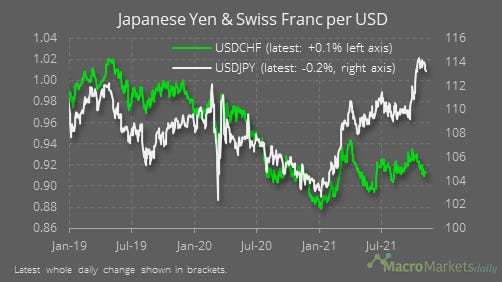

The slowdown in Japan may help to explain why the yen has diverged from the Swiss franc recently.

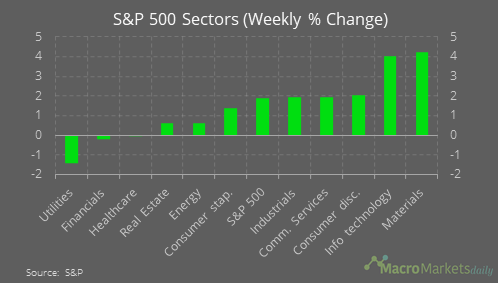

Markets appear more focused on the improving growth signs in the US, which the materials sector leading the way in the past week.

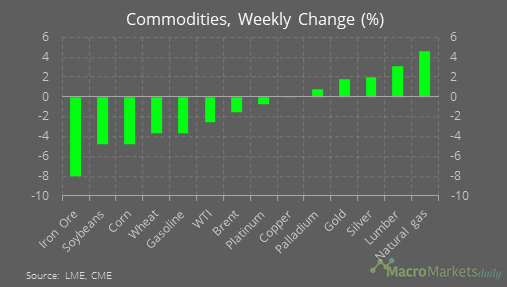

That’s despite some further falls in some key commodity prices.

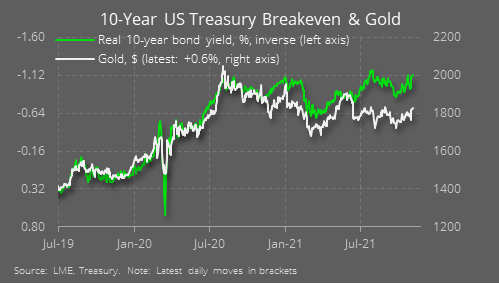

Gold and silver have been helped by the latest decline in real bond yields (inverse axis on this chart).

The Baltic Dry Index has fallen by 20.7% in the past week and is down by around half since its peak, although the China containerized freight index has yet to follow.

While some cyclical stocks in the US have done well lately, a broader global risk-on index has stuttered.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily