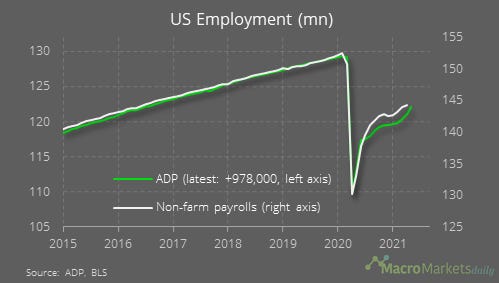

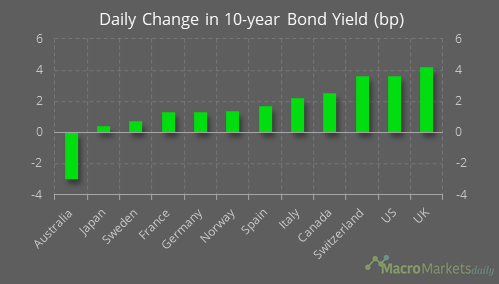

Chart of the Day

Ahead of the US non-farm payrolls report on Friday, the ADP employment report showed an increase of 978,000, which was much stronger than the consensus forecast of a 600k rise. We should take the news with some caution, given the ADP and payrolls have diverged in recent months, but the good news – coupled with other strong data releases yesterday – sent markets moving relatively sharply as investors priced in a greater chance of the Fed soon stepping on the breaks.

Macro

US initial jobless claims fell to 385,000 last week, while continuing claims increased to 3.8mn in the week before.

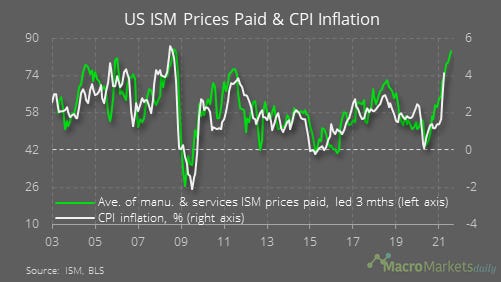

An average of the ISM prices paid indices rose in May and suggests inflation could surpass 5%.

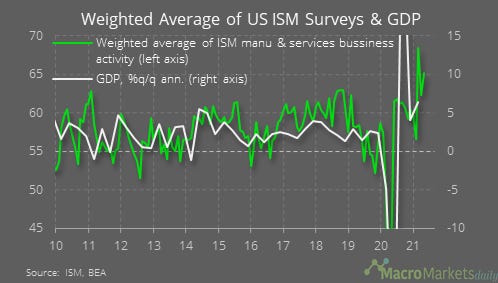

A weighted average of the ISM surveys rose to 65.2 in May, consistent with GDP growth of 10% QoQ annualized.

Markets

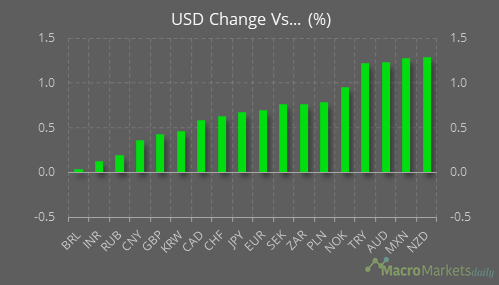

The positive US data sent the USD up against every major currency.

That was partly because the rise in yields in the US outpaced moves elsewhere.

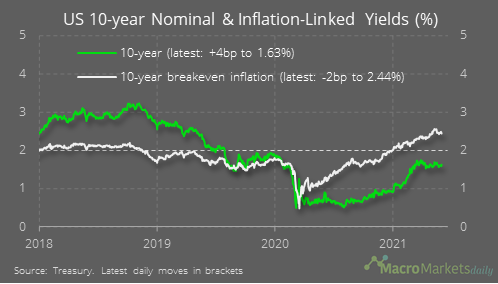

Perhaps the bigger factor was that, with the 10-year breakeven rate falling by 2 bp, the implied real rate rose by even more than the nominal rate.

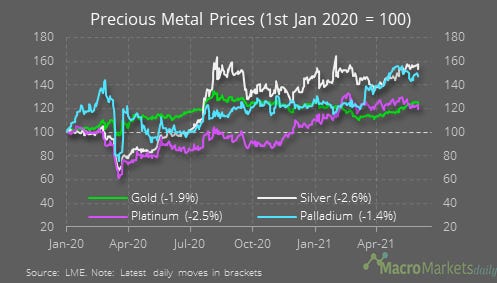

It was a weak day for the precious metals yesterday due to the rise in real yields. Moves the past week have ranged from a fall of 1.6% for silver to a rise of 0.7% for palladium.

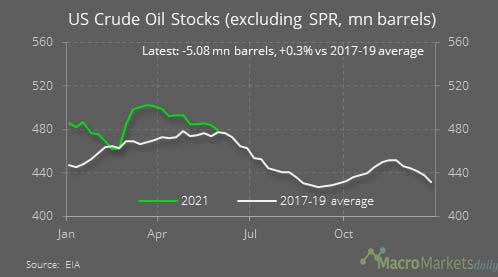

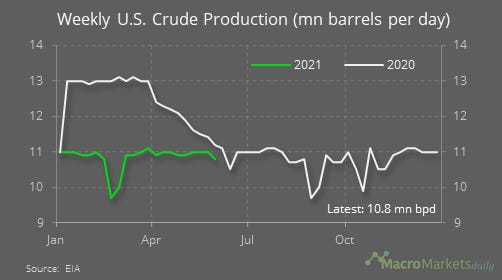

The weekly EIA report showed crude inventories fell by 5.1 mn barrels last week and are now basically in line with their norm at this time of year over 2017-19.

That’s because, while demand has been steadily rising, production has not been increasing at all and remains 2 mn barrels per day less than before Covid hit.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily