Chart of the Day

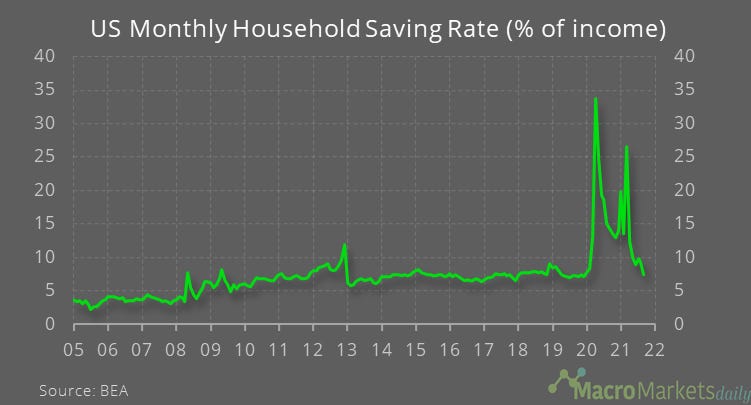

We learnt last week that US GDP growth was a disappointing 2% annualized in Q3. Most forecasters expect this to be a blip. For instance, the IMF is forecasting growth of 5.2% next year. But what if that forecast is far too optimistic? The outlook for the US is largely dependent on consumer spending, which makes up more than 70% of GDP. But the income and spending data that were also released last week showed that US household saving rate has already fallen to its pre-Covid norm. So for US spending growth to rise much further in real terms, either there must be a lot of excess savings from during the past 18 months that need to be spent, or real wages need to rise sharply. Both are questionable assumptions given much of the saving appears to have been from high-income households, who will not be in as great a rush to spend, and because the current high rate of inflation is weighing heavily on real purchasing power. Therefore, there seems to be a sizable risk that consensus forecasts for the GDP growth outlook in the US are too upbeat, and by extension assumptions for firms’ earnings growth are probably too upbeat as well – a clear downside risk to equity markets.

Macro

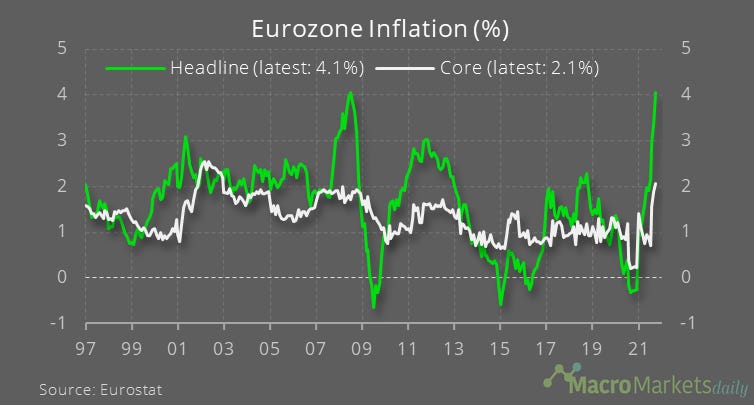

Eurozone consumers are also suffering from sharp price gains – inflation rose to 4.1% in October, while core inflation rose to 2.1%.

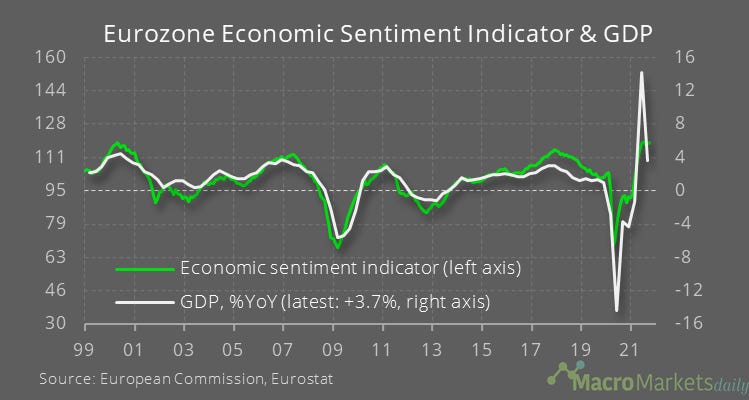

Eurozone GDP growth was stronger than in the US – the 2.2% q/q gain equates to a little under 9% annualized, although the recovery there has lagged the US so far.

The eurozone business surveys have held up quite well, but the region will suffer from the downturn in GDP growth in China to a greater extent than the US will.

Markets

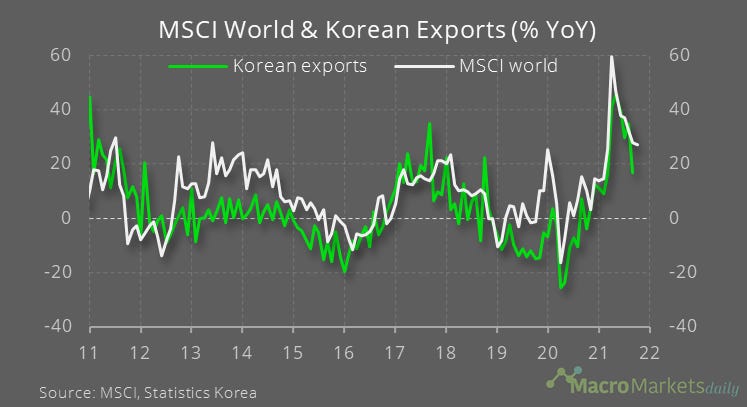

Korean exports a warning sign for global equity markets?

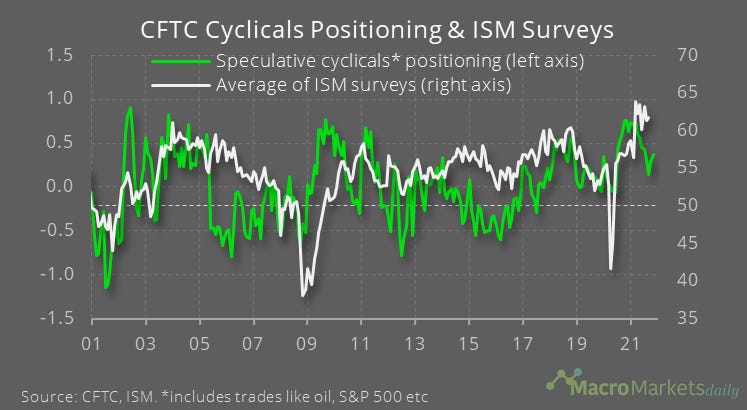

Investors don’t seem too concerned yet – speculative positioning in cyclical trades has picked up lately.

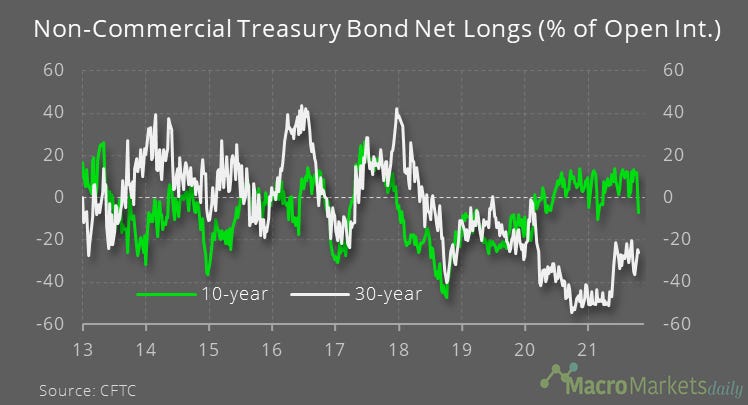

Traders are now betting outright again bonds at both the 10- and 30-year maturity, in anticipation of further yield rises.

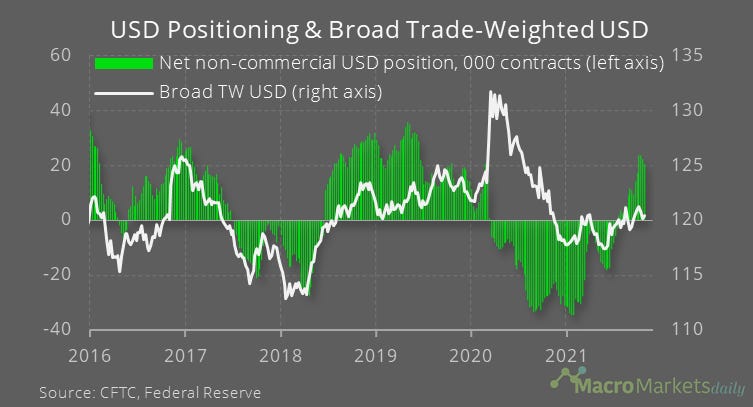

The strong USD consensus is losing some favor, with long positioning being cut again last week.

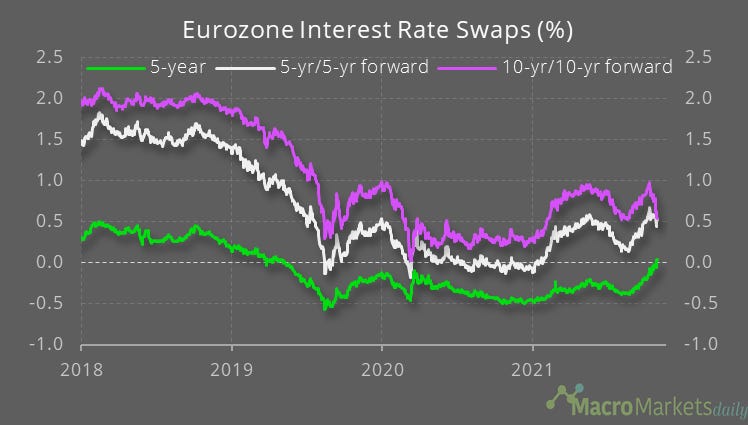

There were sharp rise in bond yields in Europe on Friday as the inflation data came in strong – one to watch for next week as potentially a downside risk to equities there.

The rise in yields mainly reflects developments at the front end, with the 5-year interest rate swap for the eurozone now back in positive territory, whereas long rates have come down sharply – basically, investors are betting the ECB will tighten relatively soon and that will keep long-rates down due to tighter monetary policy on average.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily