Chart of the Day

The big data news yesterday was that the German Ifo fell sharply and implying GDP growth there will slow sharply. As we have already seen growth slowing in China, the additional slowdown in Europe appears to be bad news for the global economy, and is something to keep an eye on given the potential negative implications for some assets including growth-sensitive commodities.

Macro

US durable goods orders fell slightly in July but are still above the pre-Covid level. Excluding transport, orders look very strong. This should sustain strong production once global supply catches up.

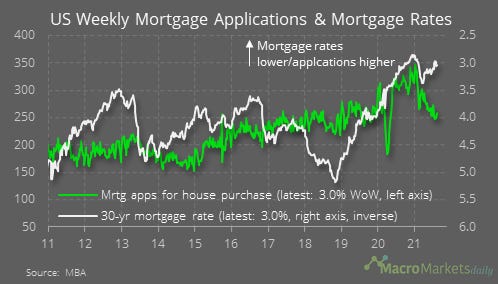

In the US, mortgage applications for house purchase rose by 3.0% last week, but have been trending down lately.

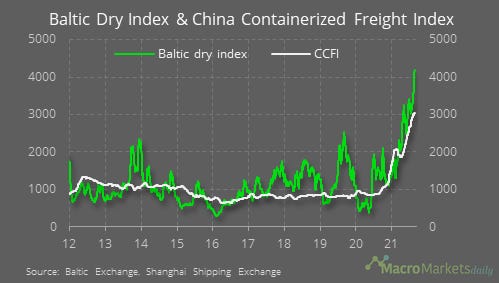

Freight rates keep rising: the Baltic Dry Index has risen by 9.4% in the past week and the China Containerized Freight Index is up by 2.3%. Is this a sign that goods inflation will remain high for a while longer yet?

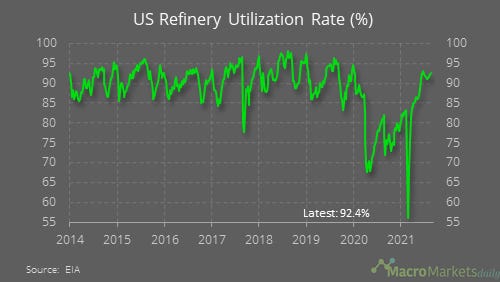

The US oil refinery utilization rate is still a bit lower than normal.

Markets

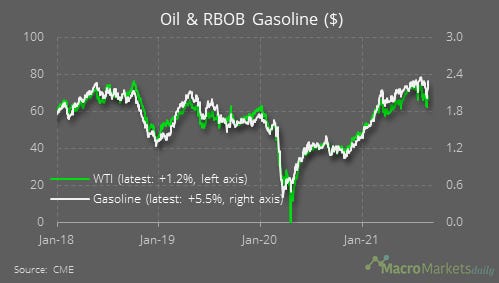

Gasoline prices far outperformed oil prices yesterday, which may have been related to the larger-than-expected drawdown in gasoline stocks in the weekly EIA report.

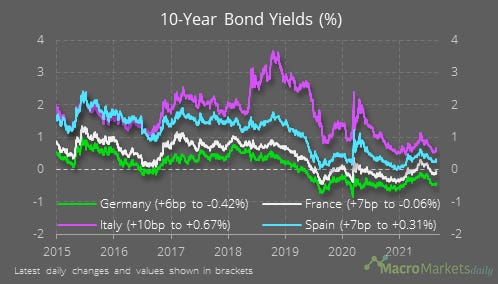

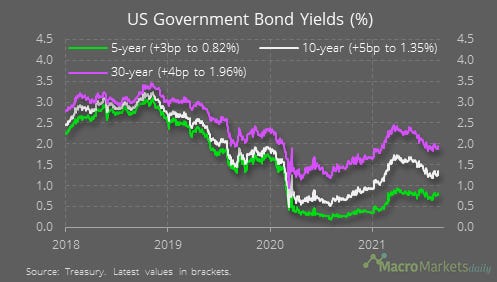

Despite the weak Ifo reading, global bond yields rose yesterday, with the gains largest in Europe. That may have been related to somewhat hawkish comments from the ECB.

The rises were not as steep in the US.

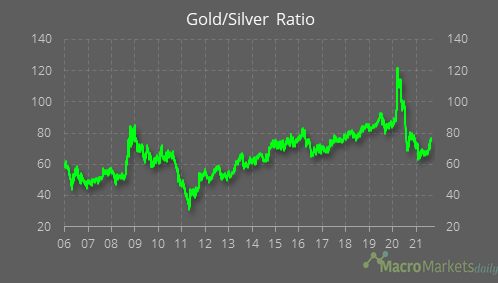

The gold/silver ratio remains below its pre-Covid level, although silver has been drifting down for the past couple of months.

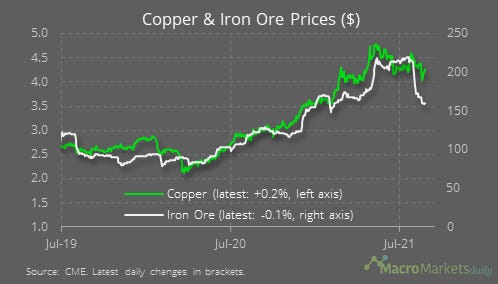

Copper prices have yet to succumb to the weakness seen elsewhere in metals markets/

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily