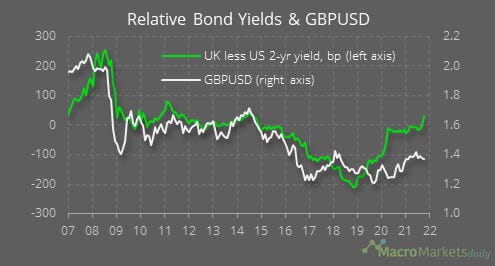

Chart of the Day

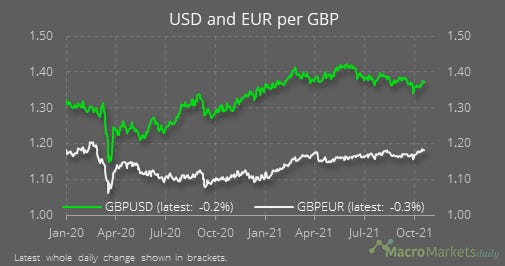

Central banks in several countries are looking more hawkish lately and there is much excitement in the UK where markets are pricing in a return to pre-Covid interest rates within the next year. That repricing has caused UK short-term yields to rise more than those in the US but the GBP has yet to show any sign of following suit. That wasn’t a huge surprise when it happened during the start of the pandemic because safe-haven flows benefitted the USD, but the disconnect looks more unusual now and could be because traders think hiking rates soon would be a policy mistake.

Macro

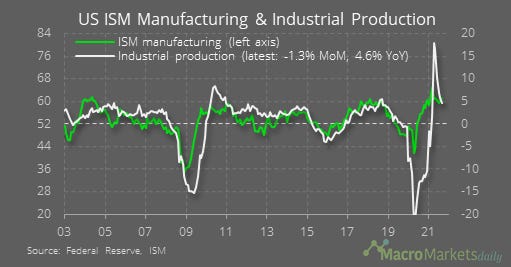

US industrial production growth decreased to 4.6% YoY in September, due to a -1.3% MoM move. Stagnation? Maybe – but there was also damage from Hurricane Ida in early September that played a role.

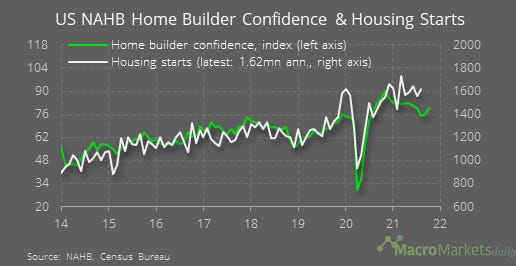

NAHB homebuilder confidence rose to 80.0 in October, though at that level it still implies housing starts could weaken.

In Canada, housing starts are now coming back down to earth.

Markets

Short-term yields continue to rise by more than those at the longer end as traders price in tightening by the Fed as well – note how the 30-year has been dropping back though, not normally a good sign for the outlook.

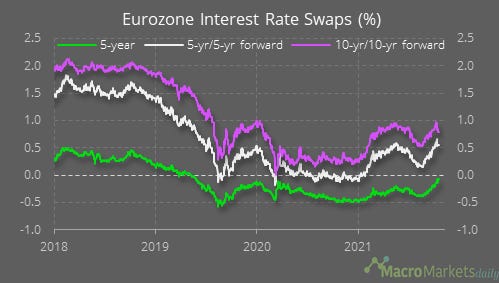

There has been a similar dynamic in the eurozone, with long-term yields still far below pre-Covid levels.

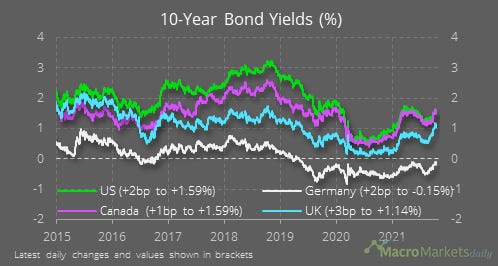

10-year yields continue to rise the most in the UK.

The 12-month OIS rate is now back to where it was before any signs of Covid were seen – an aggressive rate path considering where we were a few months ago.

Despite that move, the GBP depreciated against the EUR and USD yesterday.

It’s not just the GBP which has been moving in the opposite direction to short-term yield differentials.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily