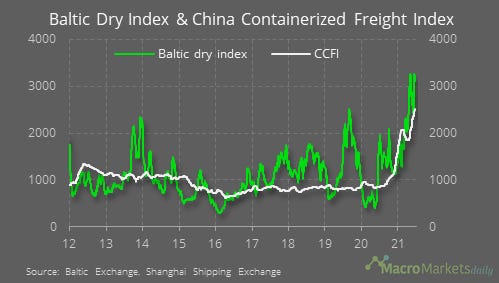

Chart of the Day

There have been some signs of declining inflationary pressures lately, for instance the sharp correction in lumber prices, but the international freight rates continue to rise – the Baltic Dry Index has risen by 3.1% in the past week and the China Containerized Freight Index is up by 3.4%. That could be a sign that further inflationary pressure is still to come.

Macro

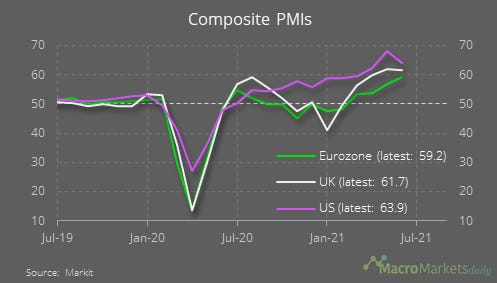

The composite PMIs for the US, eurozone and UK are converging – the June composite PMI in the US fell to 63.9, while the PMI for the eurozone increased to 59.2 and the PMI for the UK fell to 61.7.

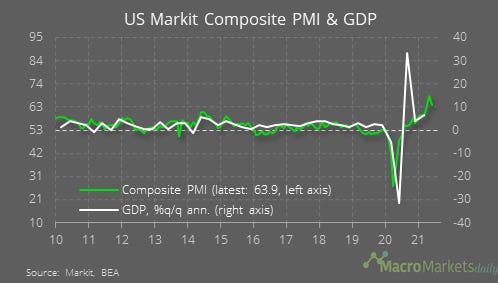

The US PMI is still consistent with very strong GDP growth.

Markets

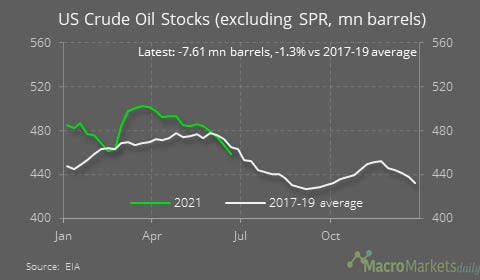

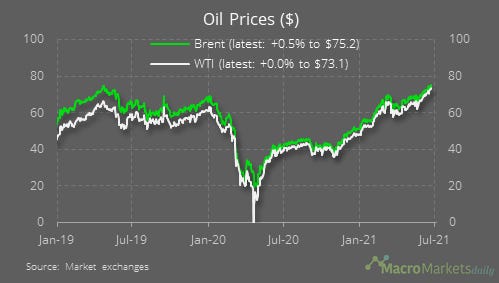

The weekly EIA report showed crude inventories fell by 7.6 mn barrels last week and are now 1.3% lower than their average at this time of year over 2017-19.

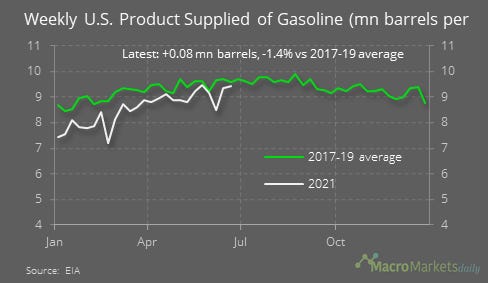

The weekly EIA report showed the amount of gasoline supplied to the market rose by 0.1 mn barrels last week and is now just 1.4% lower than the average at this time of year over 2017-19.

The reduction in inventories didn’t put a great deal of upward pressure on oil prices.

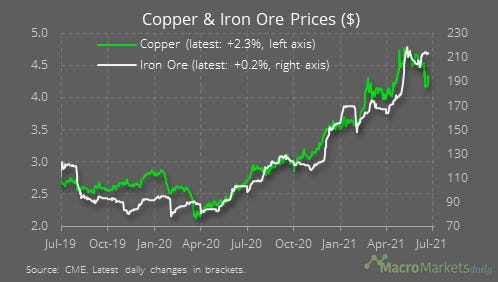

Copper rebounded yesterday, but the correction lately could be a sign the reflation trade is running out of steam.

Lumber is now down by 38.5% in the past month.

Following the Fed’s hawkish statement last week, 30-year bond yields have fallen sharply while short-term yields have risen. In other words, markets expect the Fed to raise rates by more in the short-term, which will reduce inflationary pressure and therefore the need for higher interest rates in the longer term.

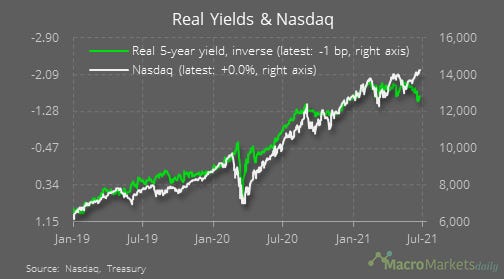

The Nasdaq has risen in the past week even though real interest rates have also increased (five-year yield line is inverted here.)

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily

Got a question? You can reply directly to this email to get in contact.