Chart of the Day

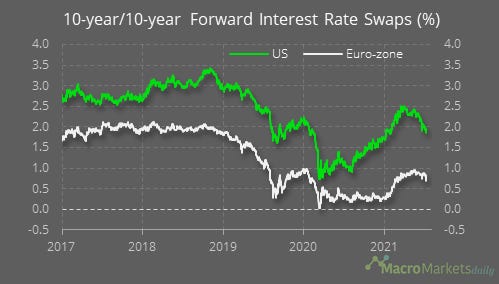

There’s been lots of talk about the potential causes of the recent declines in bond yields, ranging from concerns about the macro outlook due to poor data and new virus strains, signs the Fed might not let the economy run as hot as some thought, and technical reasons related to market structure. Whatever the cause, the move has been particularly dramatic at the long-end of the curve. The 10-year/10-year interest rate swap, essentially a measure of where markets expect interest rates to be in the 2030s, a good proxy for markets’ expectations of the policy rate that might prevail in the very long-run, has dropped back to below 2% in the US. Given it fell to that level just before the pandemic, that could be a sign that investors think the great policy experiment has changed little in practice.

Macro

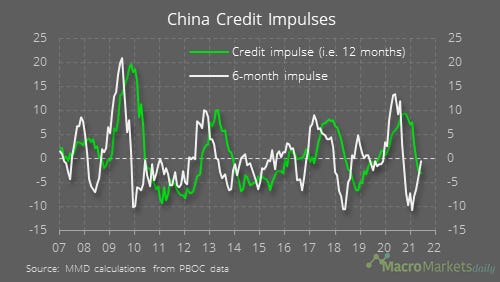

China’s six-month credit impulse has almost turned positive again, following the tightening around the turn of the year.

Wholesale inflation in India is taking off.

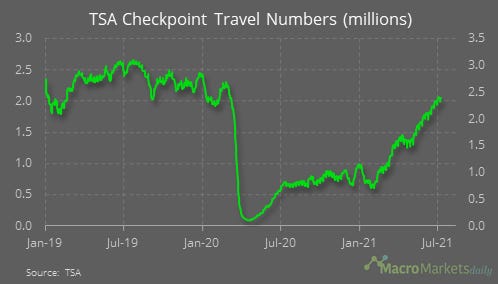

Airport travel numbers in the US are getting closer to normal.

The ECB has been expanding its balance sheet faster than the Fed.

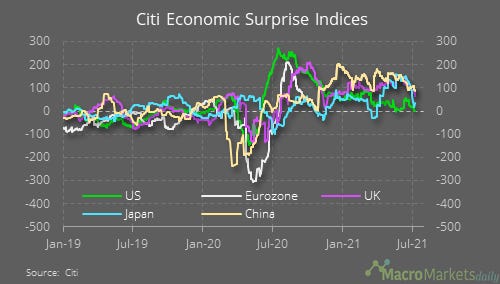

The Citi economic surprise indices have deteriorating lately.

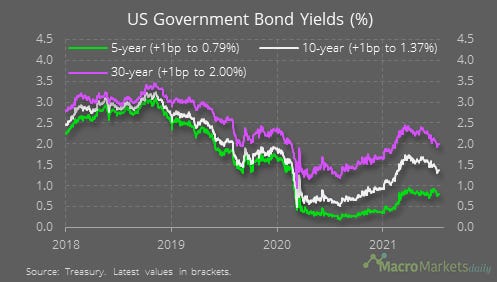

Bond yields have fallen most at the longer-end of the curve.

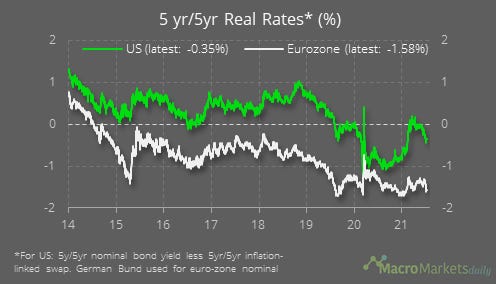

Which has caused 5-year/5-year real rates to fall by more in the US than in the eurozone.

Inflation expectations in Germany have continued to rise, but the gap with the US remains wide.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily

Got a question? You can reply directly to this email to get in contact.