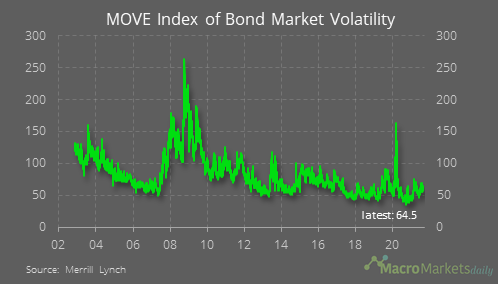

Chart of the Day

Will he or won’t he? That’s the question everyone is asking today as Powell addresses the Fed’s Jackson Hole conference and potentially hints at the Fed’s upcoming taper. The most dovish outcome is that Powell says nothing at all. Some think he might “signal that a taper signal” is to come – i.e. signal that the Fed will use its September meeting to signal that it will formally announce the tapering at the October meeting – and some think Powell could even signal that a tapering announcement will come in September. Powell has seemed more sensitive to market moves than some previous Fed Chairs, which could lean him towards one of the more cautious options. If he is more hawkish than that, then we are likely to see a rise in the MOVE index of bond market volatility, which has already headed higher in recent days after some hawkish tones from the ECB, which pushed up bond yields in Europe.

Macro

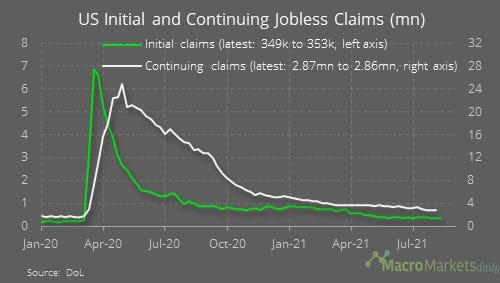

US initial jobless claims rose slightly to 353,000 last week. Economists had expected a modest rise given signs of weaker growth and the spread of the Delta variant.

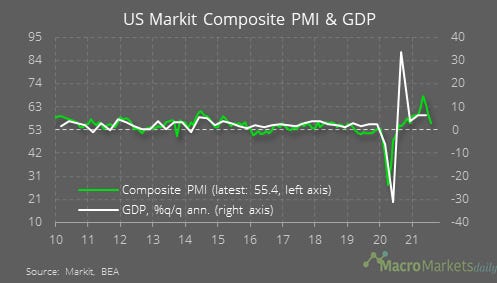

US Q2 GDP growth was confirmed at 6.6% annualized in the second release. Since then, the composite PMI has fallen sharply, signaling weaker growth.

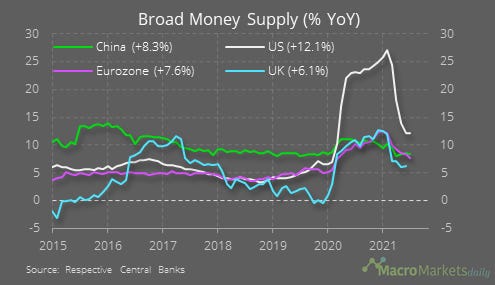

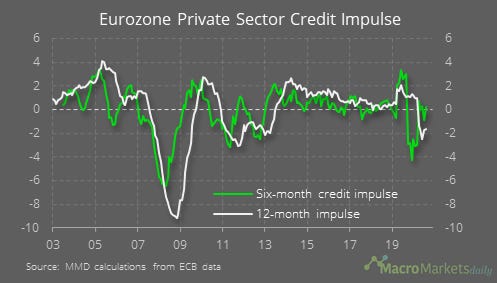

Eurozone money supply growth continued to slow in July.

The six-month private-sector credit impulse improved but is still close to zero, implying little economic boost from private-sector credit creation.

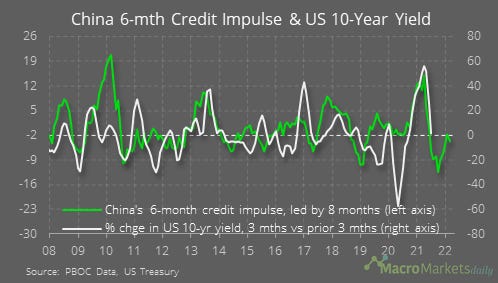

The focus is normally on China’s overall credit impulse (i.e. public and private). We learnt last week that the 6-month impulse there declined in July and remains negative.

That may have been a contributing factor to the recent declines in US bond yields.

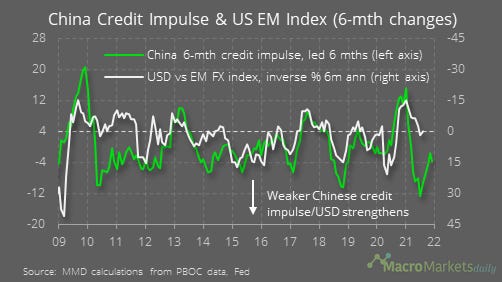

Normally a negative China credit impulse is also associated with weaker emerging market FX.

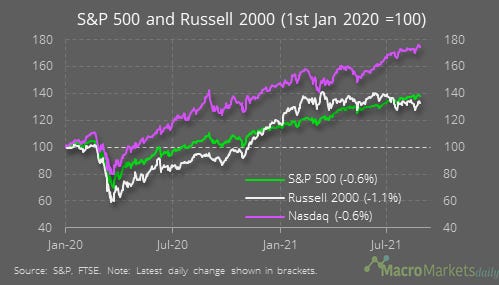

The VIX has been picking up, although the VVIX has not spiked as much as in previous episodes of rising volatility.

There was a modest equity sell-off ahead of Powell’s address although, with small caps underperforming, its not clear that is due to concerns about higher interest rates, which are normally worst news for the tech-heavy Nasdaq.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily