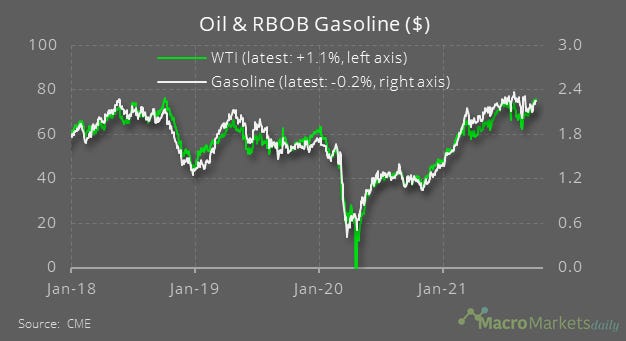

Chart of the Day

WTI oil prices rose by another 2.6% last week – not much to get excited about by itself, but still meaning that it is now less than a couple of bucks away from the $76.5 level seen in early July. Gasoline is a bit further below its earlier 2021 high, because we’re out of the summer driving season and because there was disruption to refineries earlier in the year which caused crack spreads to widen. The issue this week is how OPEC will react to recent trends. As demand looks strong, OPEC could decide to keep supply relatively tight and benefit from higher prices – some analysts say we’ll see them rise to $100 within a few months. But OPEC has been here before, and is well aware that higher prices could be the trigger required for US shale to finally start ramping up production again, which would hit OPEC market share. Which way OPEC will go is anyone’s guess…

Macro

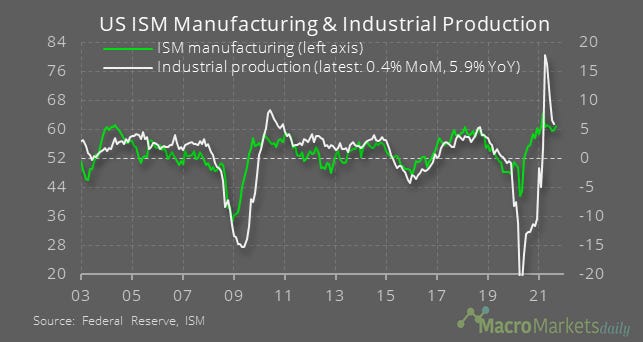

The US ISM manufacturing index rose to 61.1 in September, but that was in part because suppliers’ delivery times increased. That’s normally a good thing, because it shows demand is strong, but in this case it is because of the supply shortages. So the sector is not as strong as the ISM suggests.

Increased delivery times explain why the prices paid component of the manufacturing ISM rose in September. It suggests inflation will soon fall, but remain relatively high.

The personal income and spending data for August showed the household saving rate fell to 9.4%. If those savings are being mainly done by high-income households, there might not be much room left for savings to fall in order to boost spending.

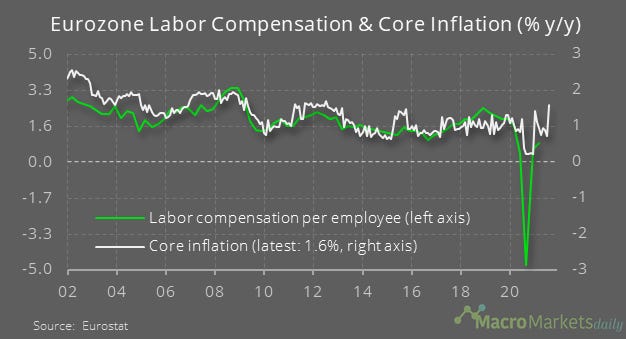

Eurozone inflation rose to 3.0% in August, while core inflation rose to 1.6%. That 1.6% rate is high by eurozone standards, but won’t be sustained unless labor compensation growth is stronger in the future than before Covid hit.

Markets

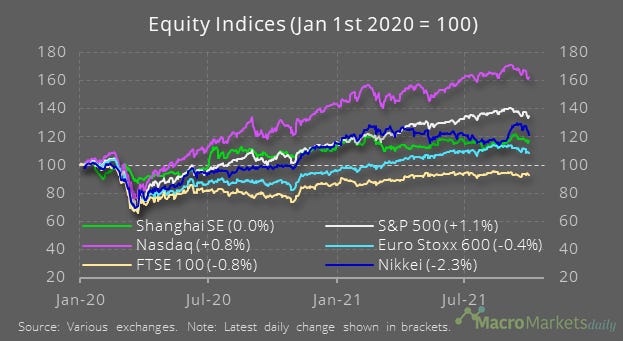

It wasn’t a great week for stocks, and it was a particularly poor week for the Nikkei, which fell by 5%. The FTSE 100 was unchanged over the week, but is still lagging in terms of its performance since 2020.

Energy has been the stand-out performer in the US, as more people focus on the opportunities from higher oil and natural gas prices.

Copper fell over the week and traders continue to shun the metal compared to earlier in the year.

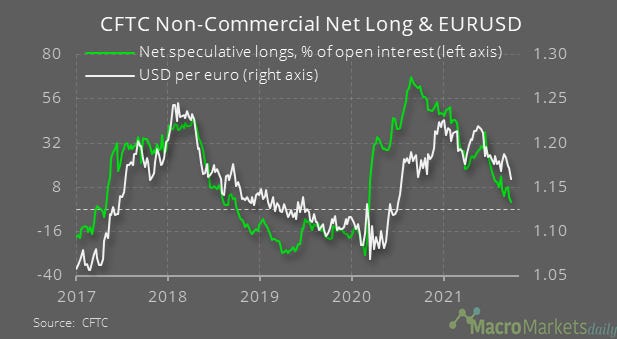

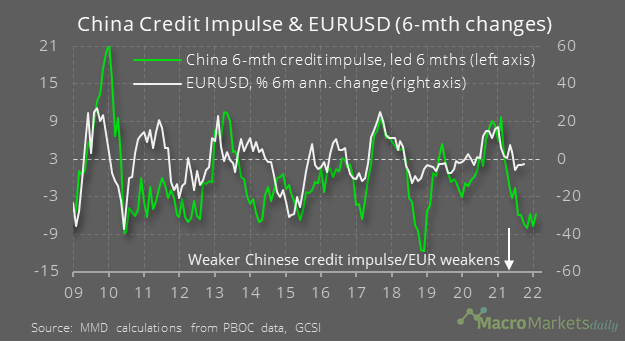

Traders are also keeping away from the euro, as it fell further last week.

That’s not all that unusual given global credit trends – EURUSD often follows China’s credit cycle.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily