Charts of the Day

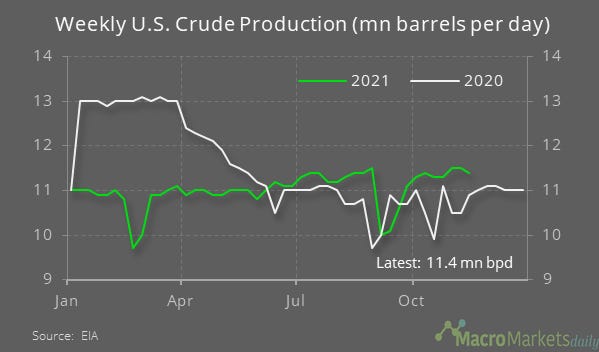

One of the key releases yesterday was the EIA weekly energy report, which showed an unexpected drawdown in oil inventories in the US. Despite the fall in inventories, WTI oil ended the day a touch lower and, importantly, fell below the 50-day moving average. The 50-day MA may not mean a great deal by itself – prices fell below the MA a few times before oil prices rallied sharply again. Nonetheless, it is still noteworthy that oil weakened despite both lower inventories and the potential technical support offered by the 50-day MA, which could be a precursor of more weakness ahead.

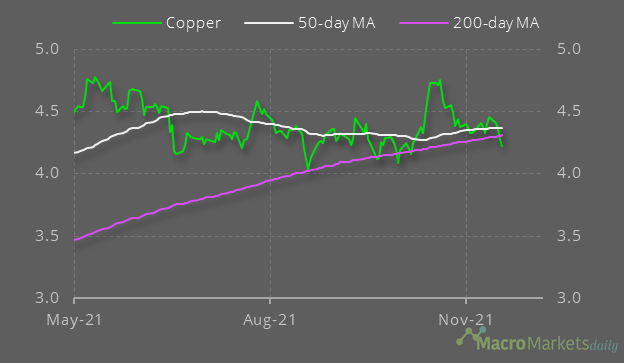

It wasn’t just oil prices showing signs of weakness either. Copper also fell further and dropped below both its 50-day and 300-day MAs. The area under the 200-day MA has acted as the previous low points for copper, so again it will be interesting to see whether there is further weakness ahead of the metal. Many believe the downturn in the Chinese property sector will hit demand hard.

Macro

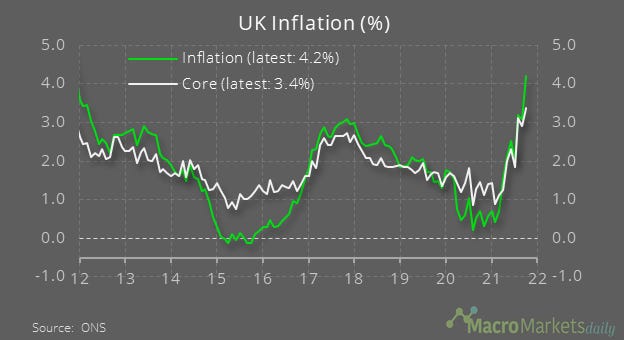

In the UK, inflation rose to 4.2% in October, while core inflation rose to 3.4%. WIth inflation now high, many expect the Bank of England to increase rates next month.

In Canada, inflation rose to an evne higher 4.7% in October, while core inflation increased to 3.8%. Again, many now expect the Bank of Canada to increase rates early next year as a result.

Markets

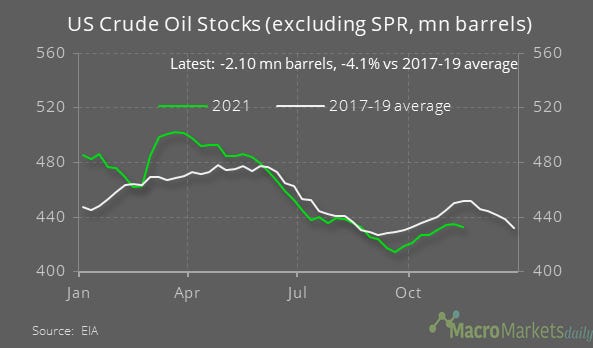

The weekly EIA report showed crude inventories fell by 2.1 mn barrels last week and are now 4.1% lower than their average at this time of year over 2017-19.

The weekly EIA report showed that US crude production fell by 0.1 mn barrels last week, despite the relative strength of prices.

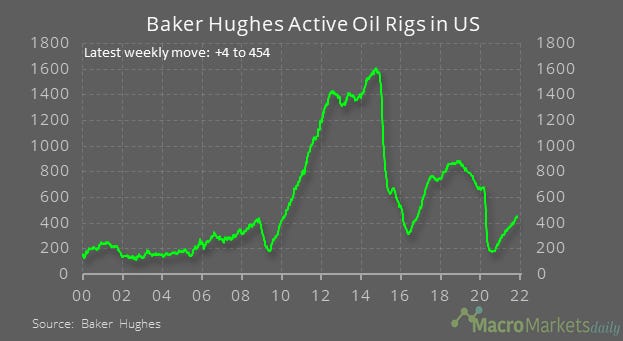

While production isn’t increasing yet, it probably will soon because the number of active oil rigs has been rising.

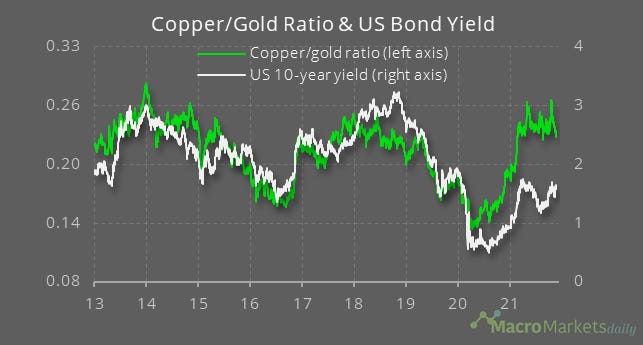

Despite the weakness of copper, the copper/gold ratio is still much higher than the historical relationship with the US 10-year yield implies.

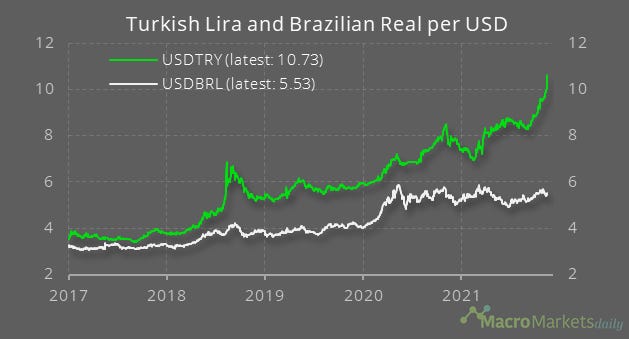

The Turkish lira has soared further and Turkey is facing some serious issues here given the impact this will have on inflation. Brazil has also been facing some major economic challenges, but its currency has done much better because the central bank has been raising interest rates rapidly.

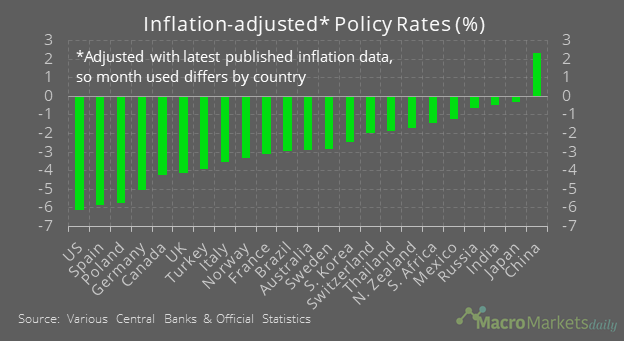

Both countries nonetheless have deeply negative real policy rates, so both central bank will probably need to do more to prevent currency weakness.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily