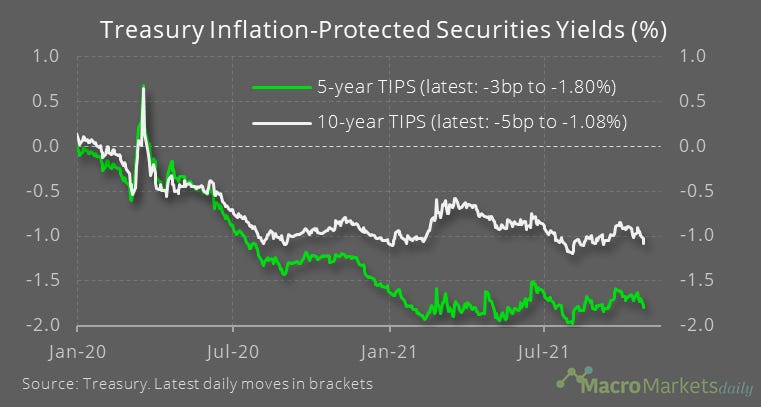

Chart of the Day

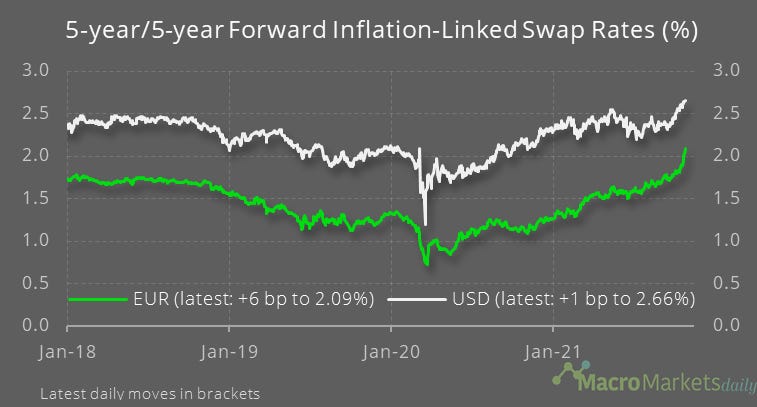

We saw yesterday that market measures of inflation expectations continue to rise in both the eurozone and US. That has pushed up nominal bond yields, but real bond yields in the US have dropped back at both the 5-year and 10-year maturity. That is one reason why tech stocks continue to do well despite earlier concerns that the Fed’s hawkish tilt would derail the stock market. Don’t get too comfortable though – the Fed tends to focus on where real policy rates are, and might not be too pleased to see them falling further when inflationary pressures are still so strong.

Macro

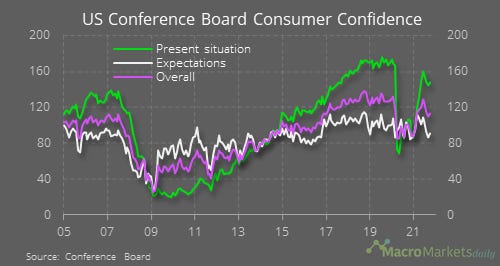

The US Conference Board measure of consumer confidence improved in October. Consumers’ expectations and assessment of the present situation both rose, but all three gauges are below recent highs and expectations are still especially low.

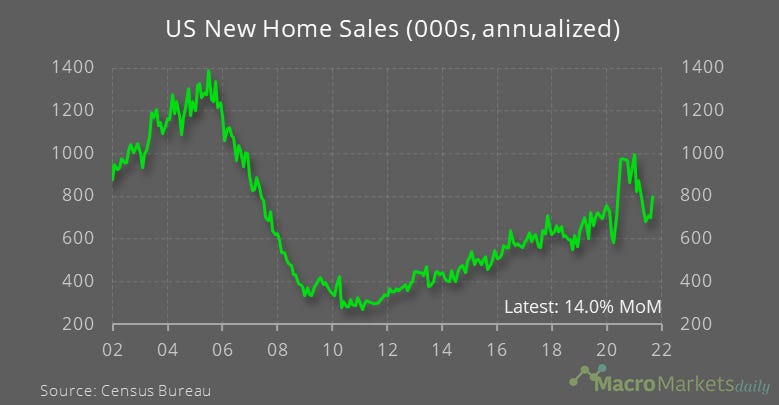

US new home sales picked up some steam and rose to 800,000 annualized in September.

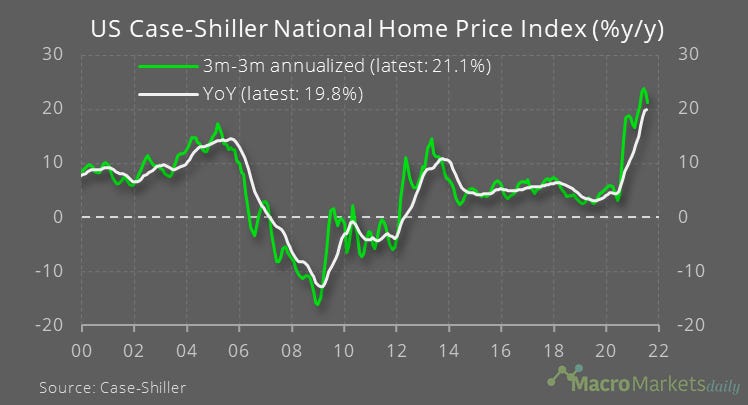

US house price inflation was little changed at 19.8% in August. The three-month annualized rate is now dropping back as momentum finally slows.

Markets

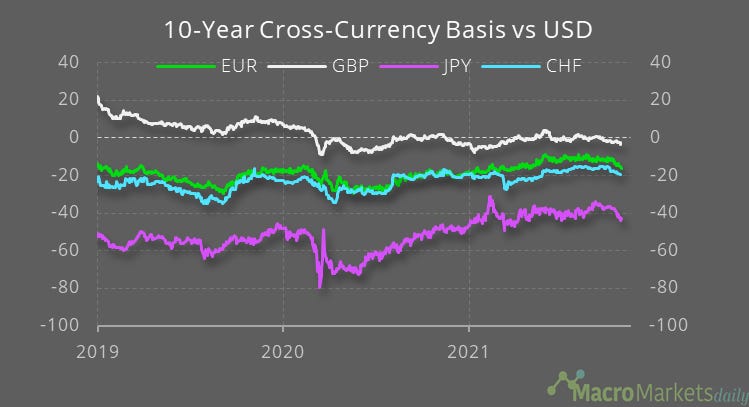

There are some signs of tighter global liquidity conditions emerging in the FX market, with cross-currency bases – the cost of transacting above that implied by interest rate differentials alone – widening against in recent weeks.

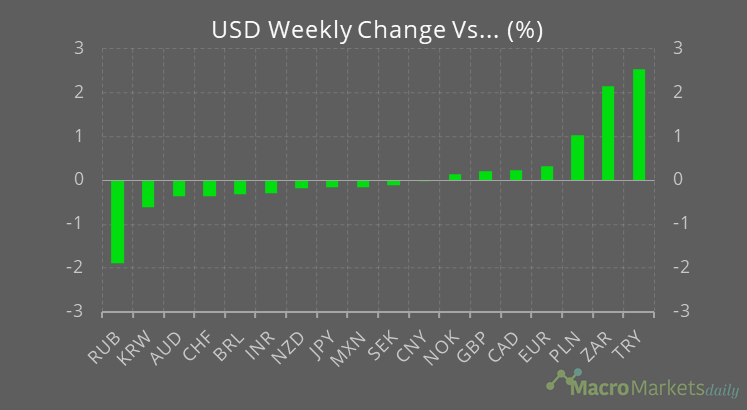

Expectations of tighter conditions may explain some of the weakness of EM currencies like the TRY and ZAR, although domestic factors are the key determinant.

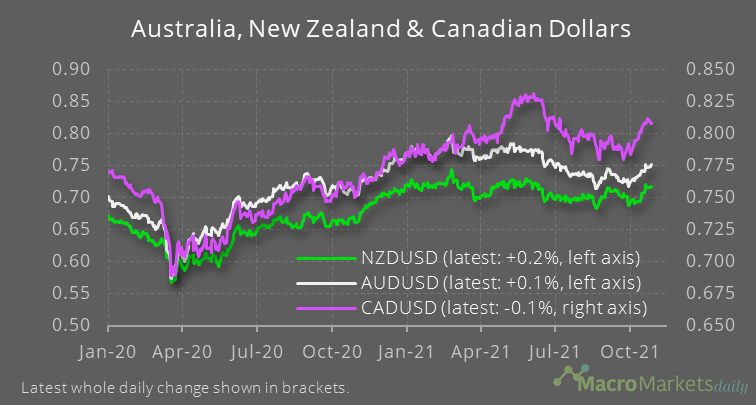

The cyclical advanced economy currencies have come off the boil after making some strong gains against the USD earlier this month.

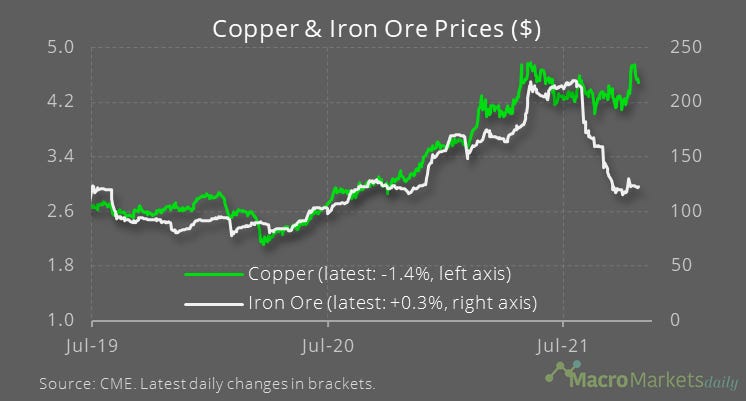

The copper market is also pulling back.

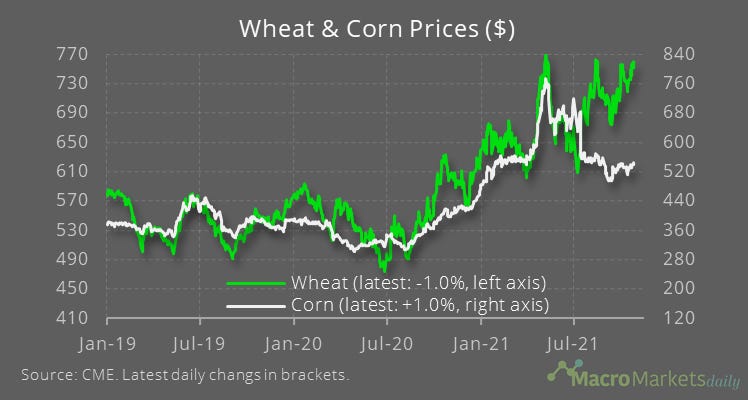

With all the talk about the impact of oil prices on inflation, one thing that is sometimes missed is the very high level of agricultural commodity prices. The inflationary impact here disproportionately affects emerging markets and can contribute toward social unrest.

Despite signs that cyclical trades are coming off the boil, the eurozone inflation swap rose by another 6bp yesterday.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily