Chart of the Day

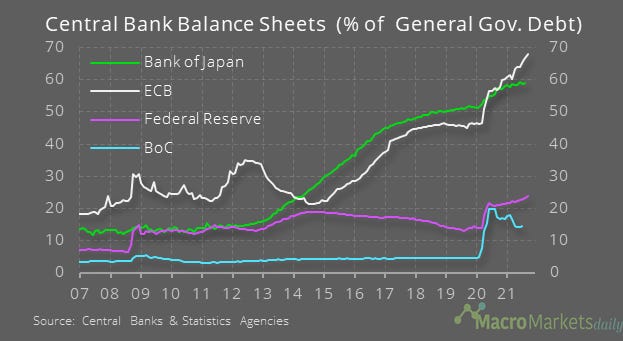

The European Central Bank confirmed yesterday that it is reducing its purchases under its emergency QE program, PEPP. Having said that, its purchases will remain relatively high and its balance sheet is likely to continue expanding at a faster pace than those of the other major central banks, especially if the Fed soon tapers itself. All these purchases have been keeping bond yields in the region very low – relative to government debt, the ECB’s balance sheet is far higher than elsewhere. If the ECB acts to keep yields very low in the eurozone, while the Fed moves to taper and eventually even raise rates, it could set up the USD for a strong run.

Macro

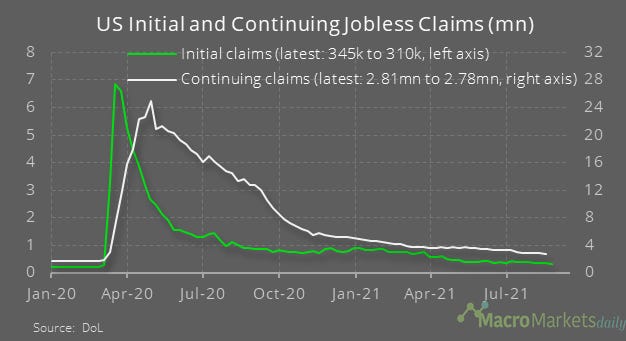

US initial jobless claims fell to 310,000 last week, but continuing claims increased to 2.81mn in the week before.

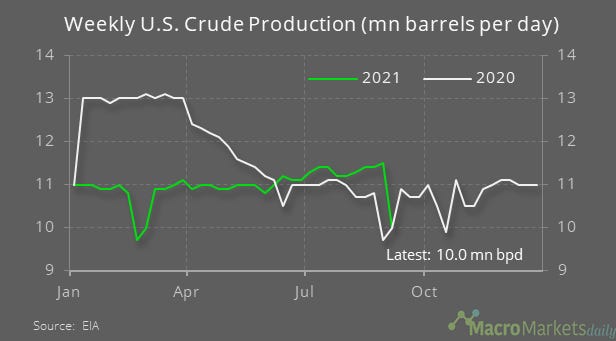

The weekly EIA report showed that US crude production plummeted by 1.5 mn barrels last week, due to the damage from Hurricane Ida.

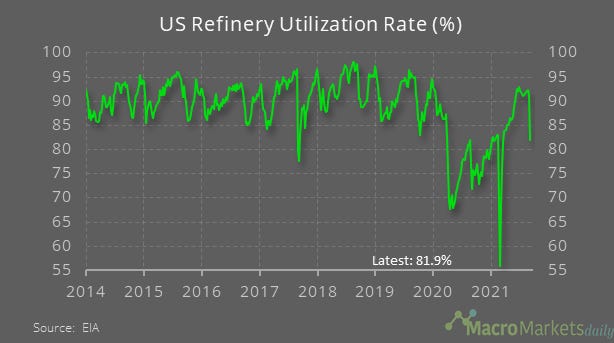

The US oil refinery utilization rate also fell sharply last week.

Markets

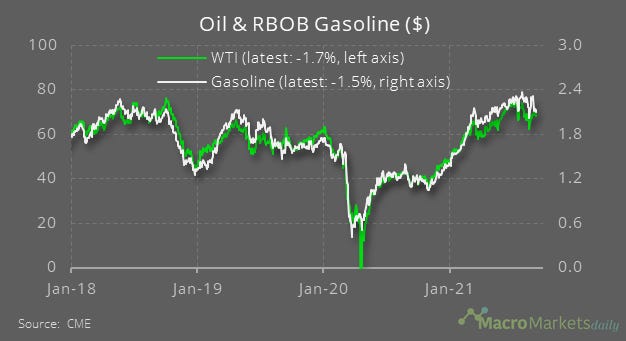

Despite lower output, gasoline prices have fallen lately.

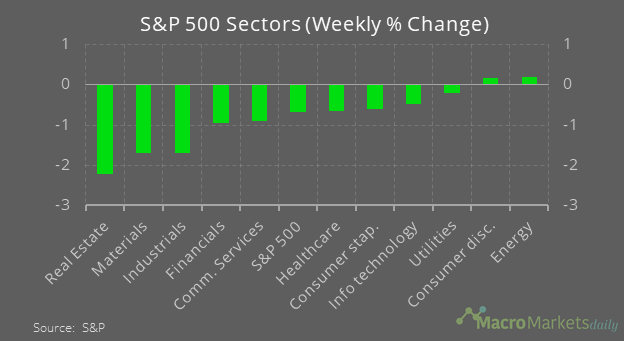

Despite only a modest rise in oil prices in the past week, the energy sector for the S&P 500 has outperformed. For most sectors, its been a bad weak, with the other cyclical sectors performing especially badly.

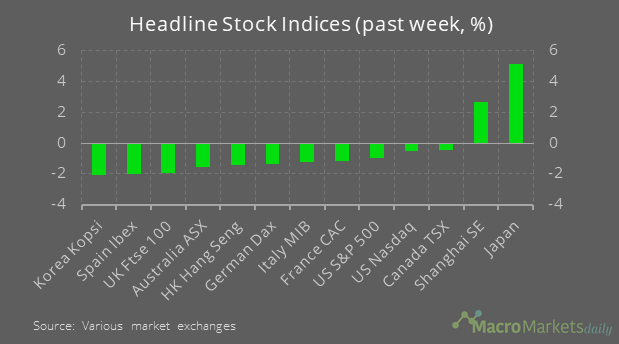

The Japanese Nikkei and Shanghai stock exchange have been the best global performers.

Bonds yields fell alongside the ECB meeting.

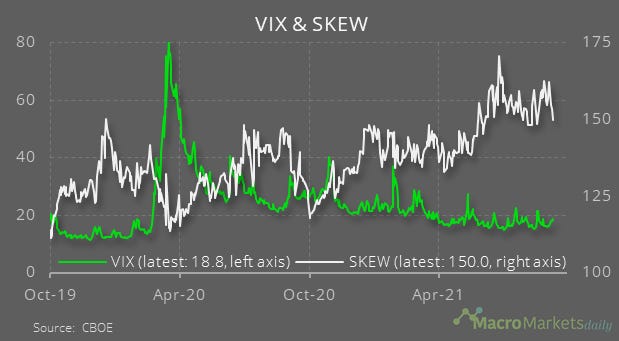

Despite the rises in bond yields until yesterday, the MOVE index of US bond market volatility has dropped back toward its recent low.

The SKEW index remains elevated, implying it remains expensive to insure against downside tail risk – mainly due to high demand for such hedges.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily