Chart of the Day

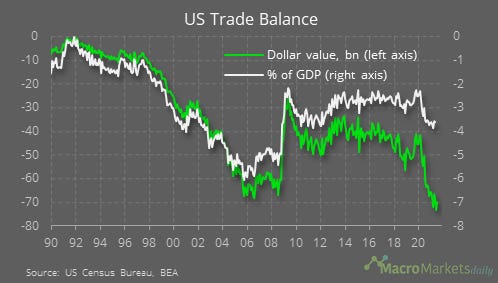

The US July trade data showed exports rose by 1.3% MoM and imports decreased by 0.2% MoM. Although that meant the trade balance improved, it remained in a substantial deficit at $70 billion, which is still larger than the previous record deficits seen before the Great Recession. While many focus on that dollar number and suggest it is a sure sign the dollar will soon weaken, the deficit is not as large if we look at it relative to GDP. It sank to 6% of GDP in 2006 but is now 3.7% of GDP.

Macro

Lay-offs in the US are now near a record low.

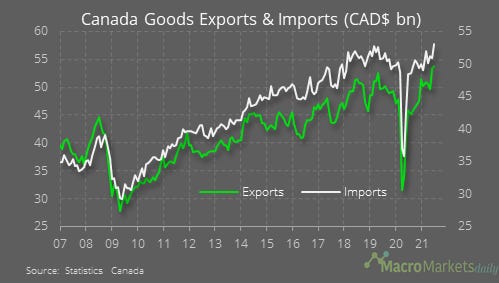

Canada’s goods exports and imports are now higher than before Covid hit. The country’s exports are benefitting from high commodity prices.

Markets

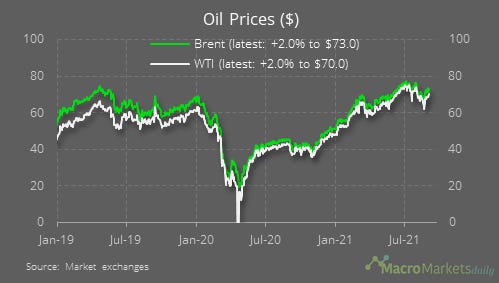

The rebound in oil prices has been especially goods news for Canada – WTI and Brent were both up by 2% yesterday, though that leaves them lower than they were in July.

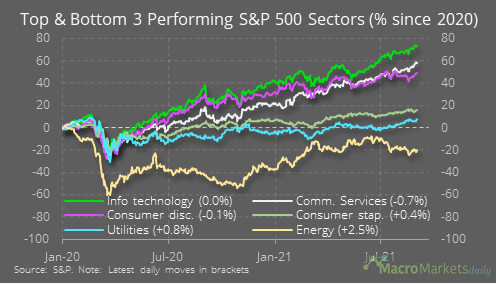

The rise in oil prices meant the energy sector outperformed yesterday. Its still lagging in terms of its post-2020 performance, as the only major sector still below the early 2020 level.

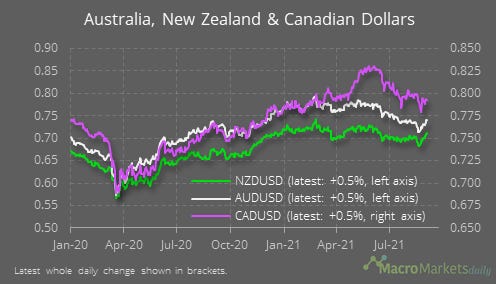

Despite higher oil prices, the CAD hasn’t match the rebounds in the AUD and NZD. The strength of AUD looks surprising given iron ore prices have slumped lately. We have the RBA next week, so traders may be betting on a hawkish meeting.

The weakness of energy equities means the sector still makes up a measly share of the S&P 500.

Tech is still dominating.

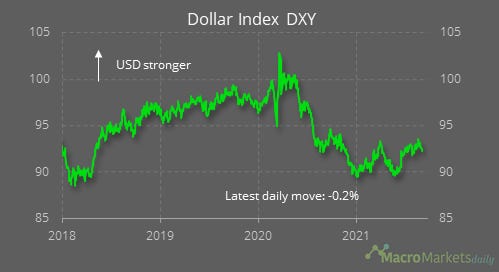

The dollar index has been heading down lately, partly as the Fed has shown little sign that a taper announcement is imminent.

Relative rates are moving against China and in favor of the US – maybe a sign the CNY is soon due to weaken?

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily