Note: Having some PC issues so we are heavy on the macro charts today and there will be no newsletter until next week at some point.

Chart of the Day

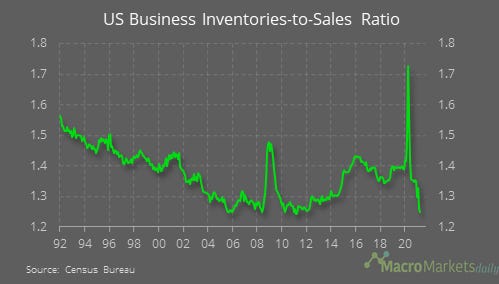

Loads of US data yesterday, and one of the less watched ones was business inventories. The data showed that the inventories-to-sales ratio fell further in April and is now far lower than in the years prior to the pandemic. Very low inventories help to explain the upward pressure on inflation and, with no end to supply chain constraints in sight, that upward pressure could continue during the remainder of the year.

Macro

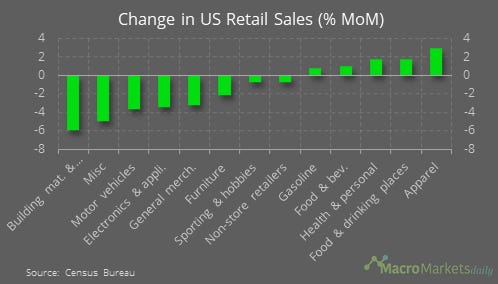

US retail sales fell by 1.3% MoM in May. The weakness has been driven by big-ticket items like vehicles and electronics. Hard to tell if that’s a sign that spending is already dropping back despite high household saving, or if it reflects supply constraints.

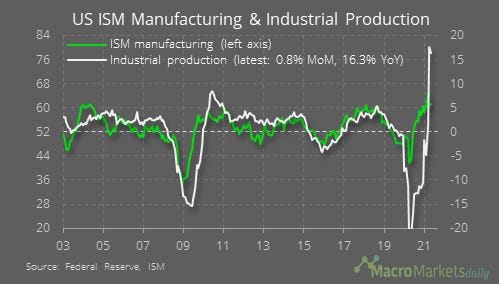

US industrial production increased only slightly, by 0.8% MoM, though the YoY rate remains high due to the comparison with last year’s lockdowns. The level of production is being held back by microchip shortages, which are affecting vehicle production especially.

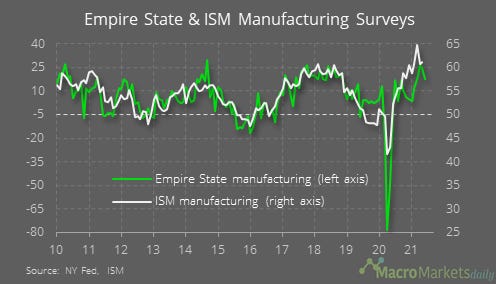

The Empire State manufacturing survey fell to 17.4 in June, which could put downward pressure on the ISM manufacturing index this month.

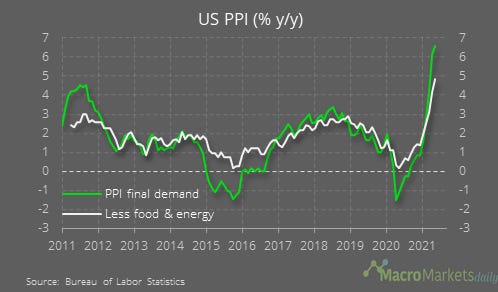

US producer price inflation rose to 6.6% in May, while core PPI inflation increased to 4.8%.

The eurozone goods trade balance fell to 1.0% of GDP in April, as exports dropped while imports rose. Again, that seems to be related to disruption to the export engine of the continent, Germany.

Canadian housing starts remain very high compared to before Covid hit.

Markets

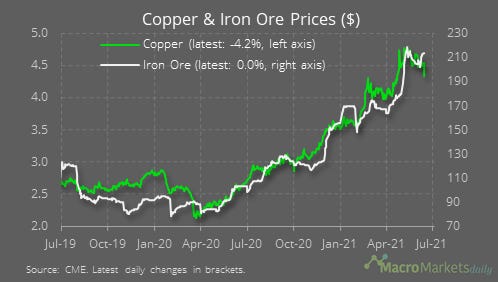

Copper and iron both fell yesterday. Copper is now down by 4.9% in the past week, and has broken down through its recent uptrend – a potentially worrying sign that further falls could be ahead, which would not be a good signal for the relation trade.

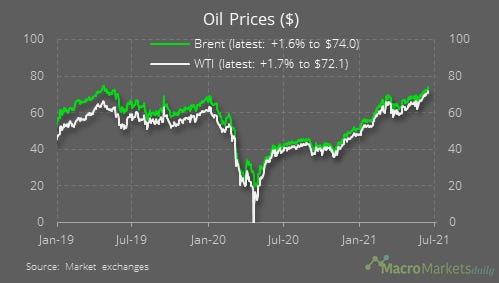

Oil prices are still sending the opposite signal; WTI rose sharply yesterday, to $72.1. Over the past week, it is up by 3.0%.

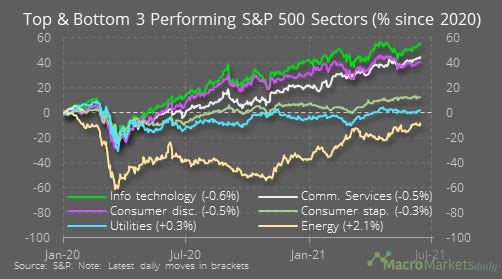

That’s helped support the energy sector of the S&P 500, though it is still the worst-performing sector in terms of its post-2020 performance.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily

Got a question? You can reply directly to this email to get in contact.