Chart of the Day

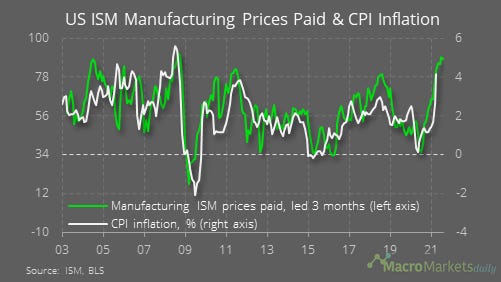

Ok, so it wasn’t a big fall, but the very small decline in the ISM manufacturing prices paid component could be a sign that inflationary pressures are finally topping out. Don’t get too comfortable yet though – it is still at a very high level, consistent with inflation of above 4%, and we need to wait for the ISM services price component before we get a complete picture of overall inflation conditions.

Macro

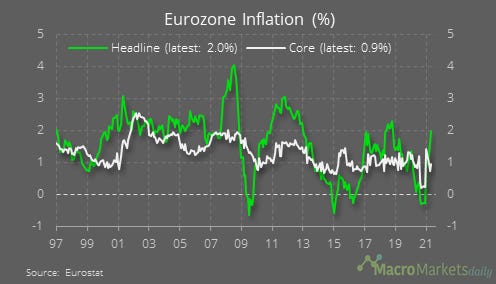

In the eurozone, inflation rose to 2% in May but core inflation remained very low.

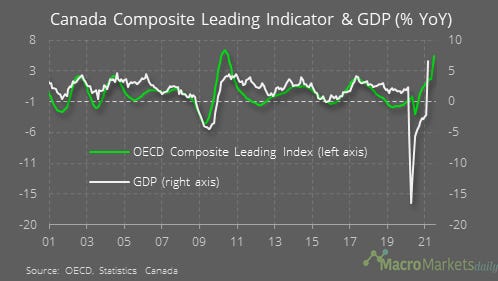

GDP rose by 1.1% MoM in Canada in March. The YoY rate jumped due to base effects.

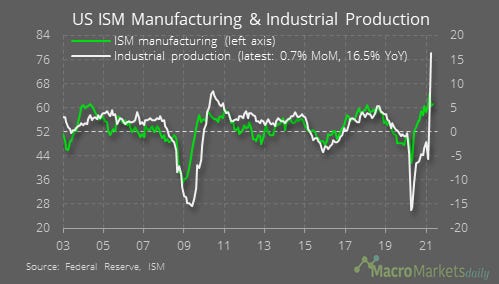

The overall ISM manufacturing index edged up in May.

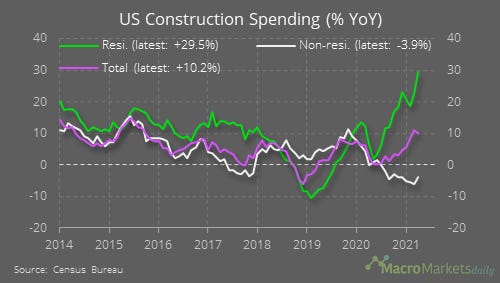

Residential construction output is booming.

Markets

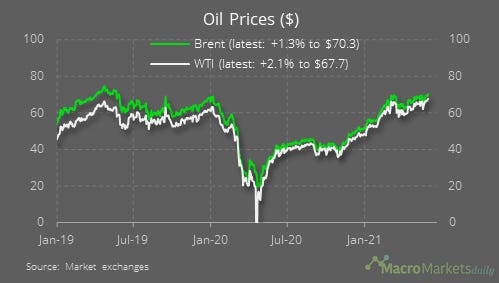

Oil prices rose to a new pandemic high after OPEC decided not to increase production. Will this be a false breakout or has the move got legs?

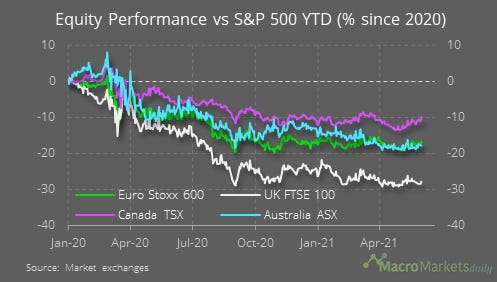

The rise in oil helped Canada’s TSX outperform yesterday – though its performance relative to the S&P 500 is similar to where it started the year.

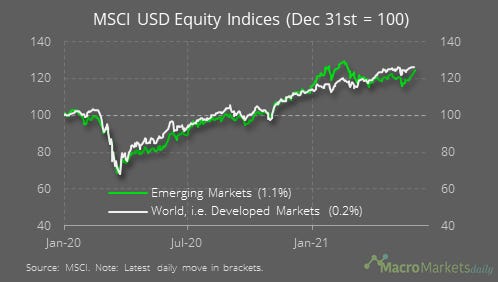

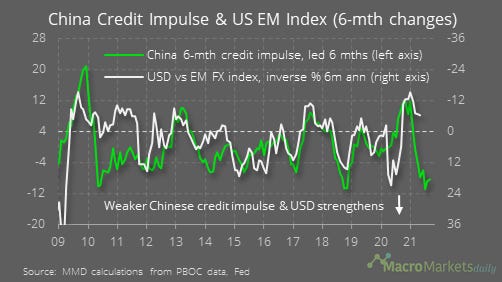

EM indices have made a more convincing rebound.

That positive sentiment has been evident in rising EM currencies, apart from the further falls in the TRY.

One reason for caution is that China’s credit impulse points to weak EM FX rates, not stronger ones.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily