Chart of the Day

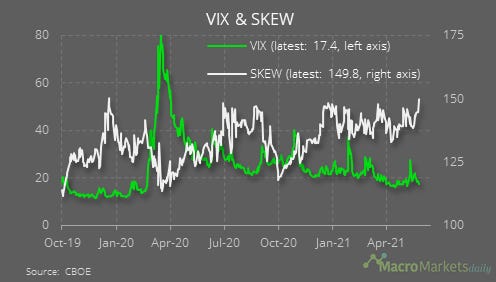

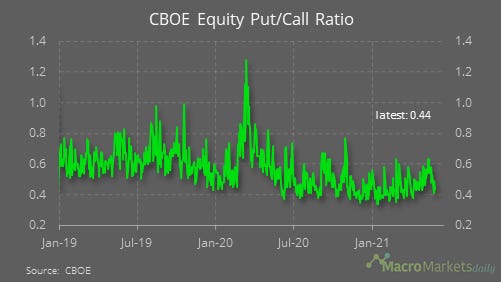

There are some signs that investors are concerned about an upcoming market correction. The VIX index of implied volatility for at-the-money options has continued to decline, but the SKEW index, which is based on deep out-of-the-money options, has jumped to its highest since before Covid. That implies investors are increasingly seeking protection against a steep fall in prices, although it hasn’t been matched by other indicators like a rise in the put/call ratio (see below).

Macro

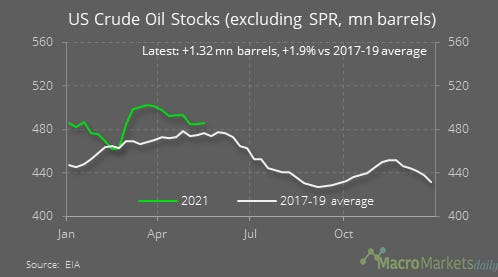

The weekly EIA report showed crude inventories rose by 1.3 mn barrels last week and are now only 1.9% higher than their average at this time of year over 2017-19.

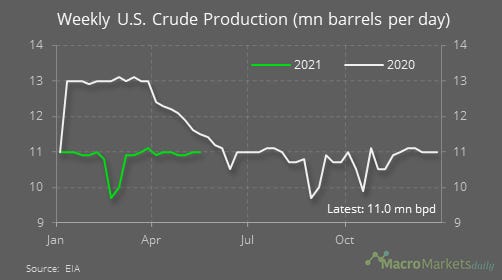

Nonetheless, higher than normal inventories continue to keep a lid on production.

The US oil refinery utilization rate was little changed last week at a relatively low level.

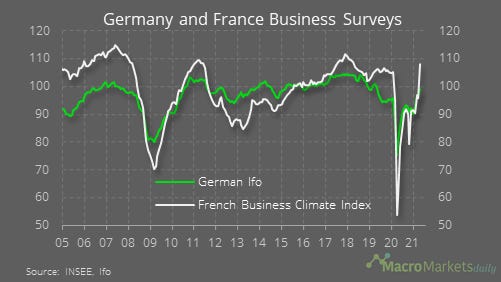

The main German and French business surveys both rose in May, with the French one leading the way and now above the pre-Covid level.

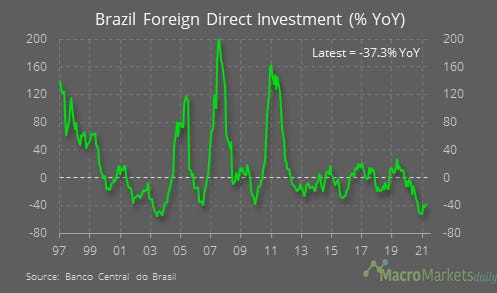

In Brazil, growth in foreign direct investment remains weak.

Markets

Like the rise in Skew, it could also be a concerning sign that a selection of assets that typify risk-off trades has risen in the past week, while risk-on assets have dropped back – not a good sign for relative positioning.

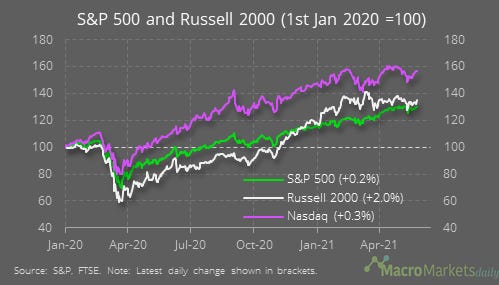

No one told small-cap investors though. After featuring the Russell’s underperformance as the Chart of the Day in the previous edition of the newsletter, the index naturally outperformed by a long shot yesterday.

Similarly, the CBOE US equity put/call ratio is still low at 0.44, compared to the long-run average of 0.62

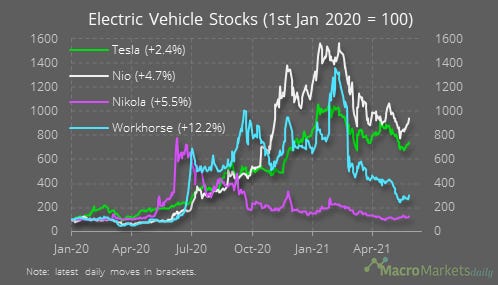

The EVs have been rebounding.

Like what you see? Please forward this email to your friends and colleagues, or use the button below to share it on social media. They can also follow us https://twitter.com/macro_daily